Editor’s note: Welcome to the final installment of our 12-part series — “Small Business Guide to Reducing Your Tax Burden Legally.” Admittedly, this final installment is technically outside the scope of this series in that it has little to do with saving money on taxes. However, it does have a lot to do with keeping more of the money you earn as a small-business owner.

Another difference is that we recruited a contributor to write this post — Jen Rodriguez, a Southern California-based forensic accountant with a Master of Accountancy and more than 20 years’ experience in accounting, operations, and data management. Rodriguez is also a graduate of Florida Atlantic University’s Forensic Accounting, Digital Forensics, and Data Analytics master’s program.

Protecting Your Business Against Theft, Embezzlement, and Fraud

By Jen Rodriguez, MAcc

Today’s headlines are filled with stories about small-business fraud, but a vast majority of these stories are about small-businesses committing fraud against the government. Most recently, the news media have focused on fraud involving the Paycheck Protection Program (PPP) — the federal government program designed to keep small businesses solvent during the coronavirus pandemic. The PPP provided ample opportunity for con artists and dishonest small-business owners to defraud the government — and you, the taxpayers — of millions of dollars.

What you hear much less about are the far more common crimes against small businesses, many of which are committed by trusted employees. These crimes include the following:

- Theft: Stealing money or property from the business outright.

- Embezzlement: Diverting money or property from the business for the employee’s own personal use.

- Fraud: Tricking a business into “voluntarily” giving away money or property.

These crimes cut into the profits of any business, but they can be especially devastating to small businesses, and are more difficult and costly for those small businesses to protect against and recover from. In this post, I look at the high costs of these workplace crimes (often referred to as occupational fraud); suggest ways that small businesses can protect against, detect, and recover from these crimes; and highlight the importance of retaining professional services when necessary.

Recognizing the High Costs of Theft, Embezzlement, and Fraud

The U.S. economy is built on the backs of small-business owners, who collectively account for $8.5 trillion dollars of the country’s $17 trillion Gross Domestic Product (GDP). Unfortunately, as we all know, money attracts thieves, and small businesses are often the easiest targets.

Criminal schemes targeting small businesses rarely attract public attention and often go undetected for many years. That’s no surprise given the fact that crimes targeting small businesses are often inside jobs committed by trusted employees. In fact, employees are stealing more than employers are aware. Recent statistics on employee theft reports that 75 percent of employees have admitted to stealing from their employer once, and 37.5 percent have stolen twice.

To protect their businesses and their own financial health, small business owners must implement comprehensive approaches to protect, detect, and recover in the unfortunate event they fall victim to occupational fraud. Problem is, they seldom take the necessary steps. Limited resources, lack of education in business operations, and limited staff and expertise restrict many business owners from establishing effective control measures. Unfortunately, it is not until after the money goes missing that they appreciate the importance of control measures.

The aftermath of fraud is long-lasting — it affects the owners personally, professionally, emotionally, and financially for years after the fraud occurs. The biggest regret small business owners have is that they hadn’t taken preemptive measures. While the effects of fraud are difficult to withstand, realizing that preventive measures could have prevented the loss is especially agonizing.

Small business owners endure the added stress of responding to customers’ and employees’ inquiries in a delicate manner to avoid legal ramifications or damage to the reputation of the business. The repercussions of fraud cause victims to feel vulnerable, exposed, and apprehensive. These feelings are intensified for business owners as they navigate through unfamiliar territories when deciding how to proceed with fraud charges and legal processes.

Learning to identify the red flags will help you detect occupational fraud and start the investigation process sooner. Losses will be reduced and small businesses like yours will have a better chance of withstanding the financial impact of the theft.

Increased Risks for Small Businesses

Small businesses are especially vulnerable to theft, embezzlement, and fraud. Why? Well, to be frank, if you own a small business, you’re more likely to have limited resources to perform countless duties to keep the company afloat. As profits grow, you can afford to hire employees and delegate some of the tasks, allowing you to focus on higher-level business tasks. However, your drive to succeed, which is an admirable attribute, can regrettably morph into an obsession that causes tunnel vision.

As a result, if you own and operate a small business with fewer than 100 employees, you may find yourself at risk of become increasingly susceptible to making mistakes that increase your probability of being defrauded by staff. Common mistakes include:

- Relying too heavily on employees.

- Trusting without verifying.

- Failing to implement internal controls or implementing weak controls.

In the 2018 Report to the Nations (the largest global study on occupational fraud), the Association of Certified Fraud Examiners (ACFE), identified that small businesses with 100 employees or fewer had the highest incident rate of occupational fraud and suffered the greatest monetary loss.

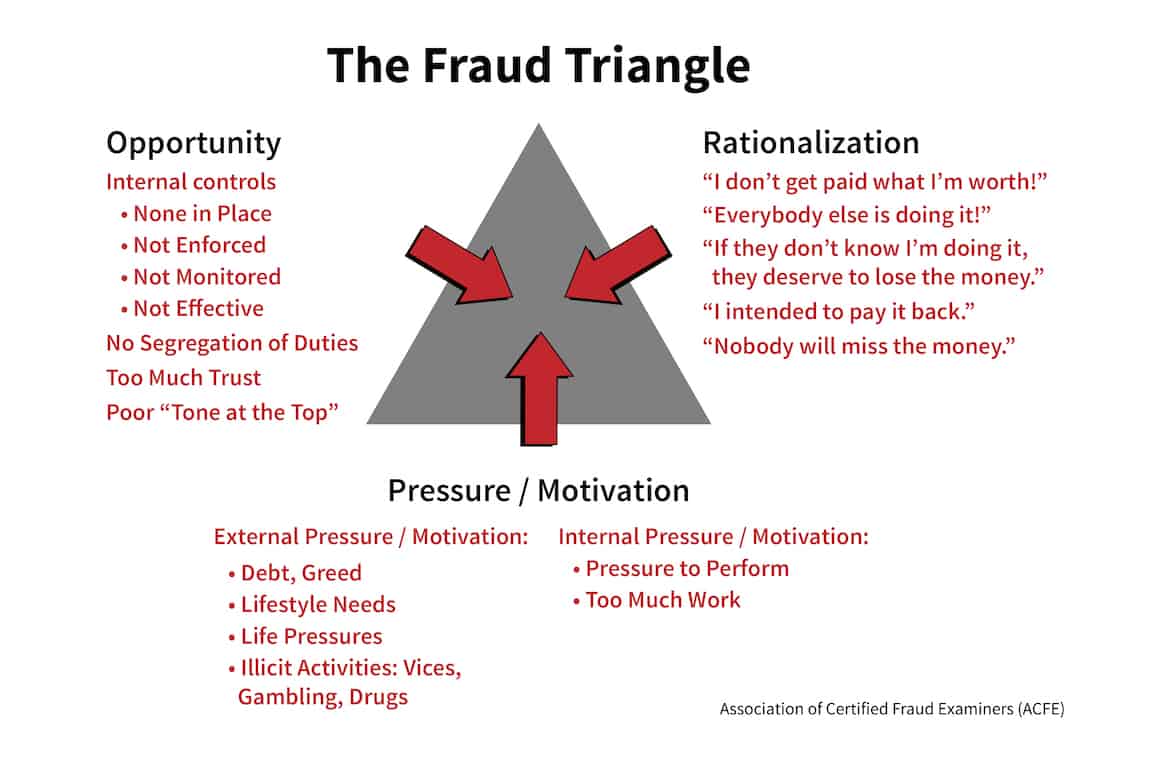

Identifying Risk Factors: The Fraud Triangle

ACFE founder, Donald Cressey, leveraged his experience as a sociologist and a criminologist to develop the fraud triangle theory, which postulates that all fraud is comprised of three criticial elements:

- Perceived pressures inside and outside the workplace

- Rationalization

- Opportunity

Keeping these three elements in sight will help you minimize the threat of fraud, especially by employees.

Unfortunately, your suffering as a result of a fraudulent act may not stop just because the fraud has been discovered. A failure to recognize the red flags of fraud is often used as defense maneuver in civil litigations as evidence of your own negligence and failure to perform a duty of care. As a result, Cressey’s fraud triangle theory is a launching pad for you to protect you and your business. Knowing your employees, paying attention to red flags, and increasing control measures are the essential first steps.

Perceived Pressures

Many of us would like to think that we would never steal from anyone, let alone our employer. In fact, according to ACFE, close to 88 percent of fraudsters have never been charged or convicted of an earlier crime. So, what drives employees to do it? First it begins with their perceived pressures, both inside and outside the workplace. The perceived pressures are commonly financial but can be nonfinancial as well. Nonfinancial pressures include unreasonable deadlines, long hours, and an unreasonably competitive work environment.

Far beyond your reach as a small business owner are the more difficult pressures such as a sick child or parent, a divorce, loss of home, or personal bankruptcy. While these pressures arise outside of the workplace, they do not remain there. They follow employees to work each and every day. By maintaining an open dialogue with employees, you can proactively find solutions to issues that otherwise could lead to resentment, entitlement, or isolation.

Employees who feel they are heard and understood are far less likely to commit fraud against their organization than those who feel they are overlooked or underpaid.

ACFE’s Cressey often refers to the perceived pressure as the fraudster’s “motive” or incentive to commit the crime. Greed is a motive that cannot be underestimated. When the rewards of stealing outweigh the consequences, fraud — or any crime for that matter — is more likely to occur. Small business owners who are appropriately aware of what is going on in the lives of their employees, will simultaneously reduce the risk of fraud and create a supportive working environment.

Pro Tip: Have an open-door policy. Be accessible to employees to hear their thoughts and learn more about what is causing their pressures, both inside and outside the workplace.

Red Flags and Rationale

Since 2008, the ACFE’s studies have repeatedly named several behavioral warning signs that are most displayed by workplace fraudsters. They include:

- Living beyond means

- Financial difficulties

- Unusually close relations with vendors/clients

- A “wheeler dealer” attitude

One red flag that is less obvious is an employee’s over-dedication to work. Simply stated, if you own a small business, you must question an employee’s unwillingness to take vacations, as well as if the employee is alwaysfirst to arrive and last to leave the office.

Nothing is out of the ordinary about small-business employees working long shifts, especially when the staff is small, but requiring employees to take time off is a strong protective measure for detecting fraud, not to mention avoiding labor violations.

Many frauds schemes are detected by accident when an employee takes a vacation and someone else needs to fill in temporarily. The typical occupational fraud scheme spans 24 months resulting in a median loss of $150,000. A two-week vacation can cut that timespan and dollar loss significantly.

Accounting and analytical irregularities are also possible indicators of fraud. That’s because small business owners are not always equipped with the skills to figure out whether inventory counts or accounting documents are correct, but an increase in accounting and software changes is a red flag that you should be able to notice.

Red flags can be subtle, but even more difficult to spot is employee rationale for stealing. People can come up with all sorts of clever reasons to justify their unethical or criminal actions. Here are some of the more common reasons employees use to justify stealing from the business:

- The company won’t miss the relatively small amount of money I’m taking.

- Other employees are doing it.

- I just needed the money for [fill in the blank].

- I deserve a lot more money than the company is paying me.

- The loss is insured.

Pro Tip: Have a tip-line or tip-box. Employees know their coworkers sometimes better than you, as the business owner, do. Allowing employees to share their concerns anonymously protects their creditability and may give you a deeper understanding of what employees are thinking or doing. The ACFE’s 2018 global study illustrates the most prominent source of early fraud detection in occupational fraud is a tip. If fact, tips are more than twice as likely as an internal audit to reveal fraud.

Also, consider having regular meetings to check-in with employees to discuss their concerns or frustrations with their workload, coworkers, or standard operating procedures. Be flexible to adapt and improve processes to increase the morale, fairness, and efficiency of your employees’ workflows.

Opportunity

In my experience, small private businesses either underestimate the importance of internal controls or lack the resources to put such controls in place. Internal controls consist of policies and procedures divided into three types:

- Preventative controls are implemented to minimize the risk prior to an incident. Segregation of duties — for example, assigning deposits to one employee and payables to another — is paramount because it creates a system of checks and balances. Segregation of duties becomes a challenge for businesses with only two or three employees and for businesses that are organized by departments instead of control measures. For example, one employee might handle the entire accounting department, giving that person full access to create fraudulent invoices, alter bank ledgers, or pocket cash.

- Detective controls are designed to identify suspicious activities. Examples of detective internal controls are surprise audits and inventory counts.

- Corrective controls are policies and procedures put into place in response to weaknesses in the system or specific incidents. An example would be when an employee discovers that his or her drawer is short at the end of their shift. One reason could be theft, but a more likely reason would be the cashier gave the incorrect change at some point. Having a procedure in place allows employees to communicate the error and implement a resolution.

Pro Tip: Make occasional inquiries to vendors to ensure the charges, the contact information, and the invoices are legit. Scan bank accounts, credit card accounts, and payment processors daily to ensure funds coming in and going out are authorized. Conduct a surprise inventory check once a quarter.

Talk with employees and ask them what controls they think are weak. By including them in the discussion, you give them a voice and an opportunity to collaborate on efforts to protect the company and, ultimately, their source of employment.

Responding to Incidents of Occupational Fraud

If you suspect one or more employees of committing occupational fraud, you want to act quickly but intelligently with full knowledge of the possible consequences of any action you decide to take. Accusing or firing an employee — even if you are certain that person is stealing from the business — could compound your problems.

With that in mind, below is one approach to consider when responding to incidents of fraud at your small business.

- First, assess the damages. Undeniably, this might further the emotional trauma of the fraud, but it is imperative. Finding out what was stolen, and the amount stolen, will help to determine how to proceed. Investigate discretely without making changes or revealing what you know.

- Don’t delay. Any delay gives the perpetrator time to discover that the crime has been detected and time to hide or destroy evidence. In addition, a delay could result in not being able to take legal action against an individual due to a statute of limitation or not being able to file a claim with an insurance company due to a limitation it has in place.

- Follow fraud-related policies. Every action you take after discovering the criminal activity will be impactful and could have profound legal and financial consequences. As a result, follow your business’s established fraud investigation policies, but if no such policies exist, consult with an attorney and/or a fraud investigator before taking any action. Ideally, hire both an attorney who specializes in occupational law and a fraud investigator or forensic accountant (FA) to work in tandem.

- Determine predication. Your fraud investigator or FA will discuss your reasons for being suspicious and help you decide whether they warrant predication (sufficient reason to launch a formal investigation). Determining predication involves reviewing “the circumstances, taken as a whole, that would a lead a reasonable, prudent professional to believe fraud has occurred, is occurring, or will occur.”

- Commence an investigation. Once predication is proven, the fraud investigator or FA will apply his or her accounting and fraud knowledge to determine the best approach to investigate the fraud and collect evidence. The investigator or FA will begin deploying various investigation tactics to collect testimonial, documentary, and physical evidence and record any personal observations.

- Prosecute (or not). Once the investigation is complete and substantial evidence has been collected, you can decide, with the assistance of legal counsel and law enforcement, how to proceed.

Make no mistake about it — and I do not mean to scare or frighten you — but occupational fraud is rampant, and it poses an existential risk to any small business owner who operates as if they’re immune to being taken advantage by their own employees. As a small business owner, you have an obligation to yourself, your family, and your business to put suitable controls in place to discourage and prevent theft, embezzlement, and fraud. You should also have policies and procedures in place to guide you in the event that such crimes occur, so you can quickly address the problem, mitigate the damage, and strengthen your controls.

Stees, Walker & Company, LLP, can help you put the necessary controls in place and recover in the event that your business falls victim to occupational fraud. They offer a range of services, including rebuilding your books, filing tax amendments to account for the fraud, and claiming any tax deductions related to losses from fraudulent activity to offset those losses. If additional legal or specialized forensic accounting services are necessary, they can refer you to reputable providers.

– – – – – – – – – –

About the Author: Jen Rodriguez, MAcc, is the Founder & CEO of Insight FCS — a Southern California-based forensic financial services firm. A graduate of Florida Atlantic University’s Forensic Accounting, Digital Forensics, and Data Analytics master’s program, Rodriguez and her colleagues at Insight FCS specialize in leveraging business data and technology to uncover fraud and accelerate business performance. To connect with Jen about this article or the work she does in the area of forensic accounting, please call or email: (949) 742-2772 / jen@insightfcs.com.

– – – – – – – – –

Disclaimer: The information in this blog post about theft, embezzlement, and fraud is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from either Jen Rodriguez, Insight FCS, or the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Jen has not only delivered the most helpful information on small business fraud, she presents it in a very easy to understand way. I will start to apply her methods right away in hopes of avoiding the pitfalls of owning a small business.

Thank You Jen

Thank you for shedding light on such crucial aspects of business protection! Your comprehensive guide offers valuable insights into safeguarding against theft, embezzlement, and fraud, providing practical strategies for business owners to mitigate risks and ensure financial security. This information is indispensable for anyone looking to safeguard their hard-earned assets and maintain trust within their organization.