The Pros and Cons of a Cost Segregation Study

Share This Post

If you own real estate, or you’re interested in investing in real estate as a strategy for building or increasing your net worth, then you need to know about cost segregation.

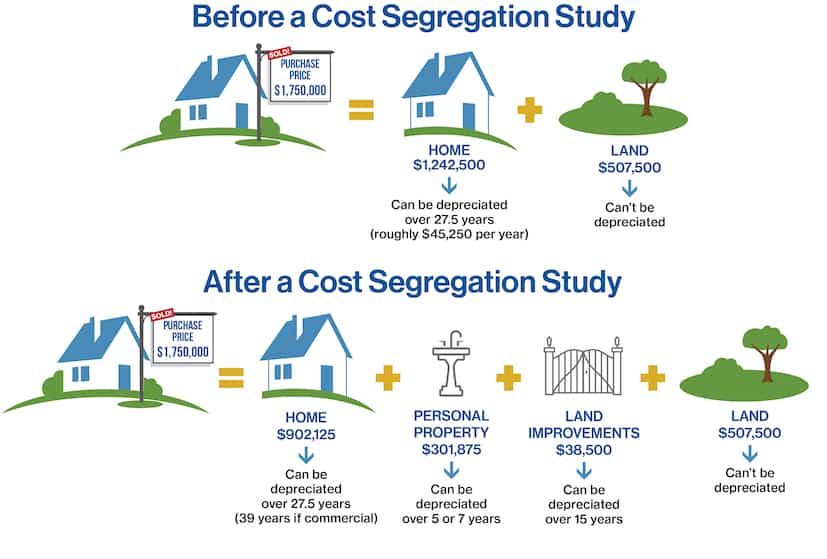

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

This reallocation can provide significant tax benefits because shorter-lived assets are eligible for accelerated depreciation.

Depreciation 101: Depreciation is an accounting technique that distributes the cost of tangible assets such as real estate over their useful lifespan. It reflects the portion of an asset’s value that’s been utilized, allowing you to gradually pay for and generate revenue from an asset over a specified period of time.

When a property is built or purchased, the costs of the property (such as construction costs or the purchase price and cost of improvements) are typically allocated to the building and land as long-term assets. However, many of the items within a property (such as carpeting, lighting fixtures, and appliances) have a shorter useful life and can be classified as personal property. By identifying these shorter-lived assets and reclassifying them as personal property, the costs associated with them can be depreciated over a shorter period, resulting in a larger tax deduction in the early years of ownership.

Starting With a Cost Segregation Study

To add cost segregation to your tax planning approach, start by ordering a cost segregation study from a reputable firm. Here at SWC, we work with several of these firms and can recommend the right one for your particular circumstances and objectives.

When you engage a firm in a cost segregation study, a cost segregation specialist identifies and reclassifies the costs of your property, typically by examining the property and its invoices, blueprints, and other documentation. The study then allocates property costs to real property or personal property. Findings from the study can then be used by your tax planning firm — in this case, SWC — to calculate a one-time catch- adjustment. That’s because the IRS allows the Continue reading… Continue reading… Continue reading…