Welcome to Part 3 of our 12-part series on how to legally reduce your income tax burden. Here, we describe the five ways you can choose to organize your small business, and then we provide guidance on how to choose the best business entity for your business in the current environment.

Here’s a common scenario to get us started. You set up a limited liability company (LLC) or S corporation for your small business, and now you are all set in terms of protecting your personal assets from lawsuits and minimizing your tax burden, right?

Not so fast.

One of the most expensive mistakes small-business owners make is choosing the wrong business entity — the legal/financial structure within which the business operates.

Most business owners start as sole proprietors. Then, as they grow, they establish an LLC to help protect their personal assets from any lawsuits filed against the business. Many of these same business owners make the common mistake of assuming that an LLC allows them to file their taxes as a corporation and use that filing status to save on taxes. The fact is that an LLC is a legal entity, not a tax entity. Operating a sole proprietorship as an LLC won’t save you any money in taxes.

You want a business entity (or more than one business entity) that not only provides legal protection, but also maximizes your tax savings.

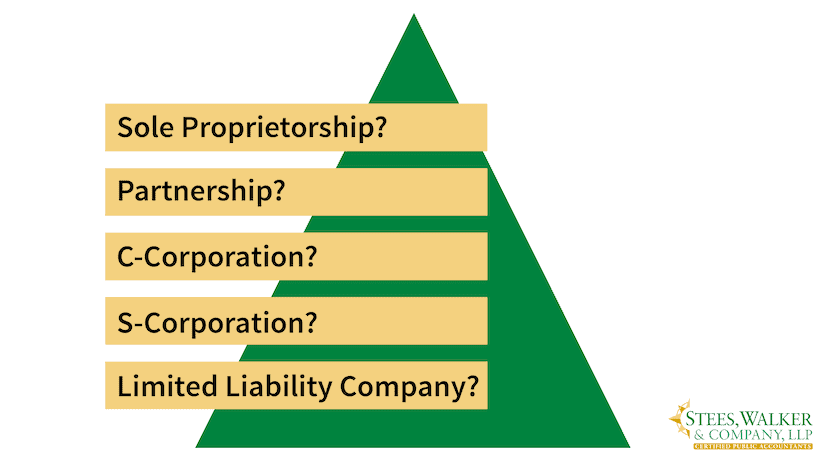

Knowing Your Business Entity Options

When choosing a business entity, you have the following five options (only the first four are tax entities):

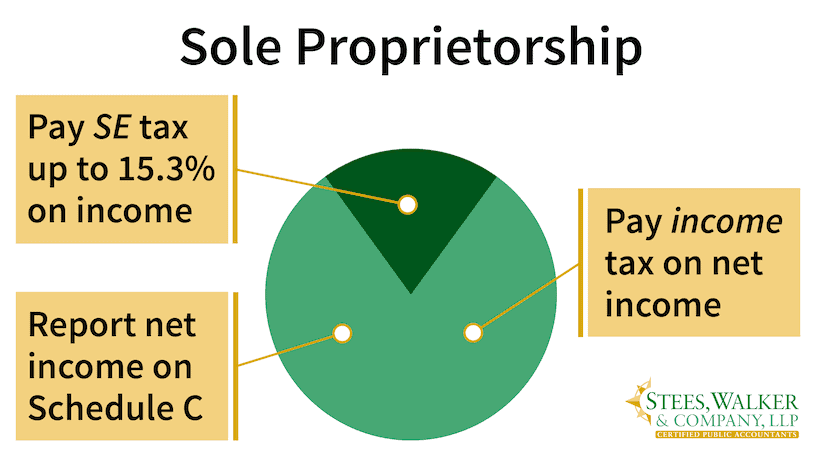

- A sole proprietorship is a business you operate yourself — in your own name or a trade name — with no partners or formal entity. You report income and expenses on your personal return (Schedule C) and pay income and self-employment tax on your profits. This option is okay for startups and small businesses with no employees, operating in industries with little legal liability. However, it is the most expensive in terms of taxes.

- A partnership is an association of two or more partners. General partners run the business and remain liable for partnership debts. Limited partners invest capital, but don’t actively manage the business and aren’t liable for debts. The partnership files an informational return and passes income and expenses through to partners. General partner distributions are taxed as “ordinary” income and subject to self-employment tax; limited partnership distributions are taxed as “passive” income not subject to self-employment tax.

- A C corporation is a separate legal “person” organized under state law. Your liability for business debts is generally limited to your investment in the corporation. The corporation files its own return, pays tax on profits, and chooses whether or not to pay dividends. Your salary is subject to income and employment tax; dividends are taxed at preferential rates and not subject to self-employment tax. This business entity is generally best for owners who need limited liability and want the broadest range of tax benefits. However, the administrative costs and complexities are also the highest.

- An S corporation is a business that elects not to pay tax itself. Instead, it pays salaries to any employees (who are responsible for paying taxes on that income), and it passes any profits to shareholders — a situation in which the shareholder is responsible for payment of the individual taxes. An S corporation is generally best for businesses whose owners are active in the business and don’t need to accumulate capital in the business to cover expenses for day-to-day operations.

- A limited liability company (LLC) or limited liability partnership (LLP) is an association of one or more “members” organized under state law. Your liability for business debts is limited to your investment in the company; in fact, LLCs may offer the strongest legal protection against the loss of any personal assets in the event someone files a lawsuit against the business. However, an LLC is not a distinct entity for tax purposes. LLC’s are considered “disregarded entities,” which means they take on the tax characteristics of the tax entity that the members choose for it to be. Single-member LLCs are taxed as sole proprietorships, unless the owner elects to have it taxed as a corporation. Multi-member LLCs can choose to be taxed as partnerships or corporations. Many small businesses operate as an LLC (for legal purposes) and a partnership or S corporation (for tax purposes).

We can’t make you an expert in business entities — at least not in a single blog post — but we do want to walk through one popular choice to illustrate how important this question can be.

If you operate your business as a sole proprietorship, or a single-member LLC taxed as a sole proprietorship, you may pay as much or more in self-employment tax than you do in income tax. One way to reduce your self-employment tax is to set up an S corporation and file your tax return as an S corporation instead of as a sole proprietor.

If you’re taxed as a sole proprietor, you’ll report your net income on Schedule C. You’ll pay income tax at whatever your personal tax rate is, along with self- employment tax of 15.3 percent on your first $137,700 of “net self-employment income” and 2.9 percent (Medicare tax) on anything above that. You’re also subject to a 0.9 percent Medicare surtax on anything above $200,000 if you’re single, $250,000 if you’re married filing jointly, or $125,000 if you’re married filing separately.

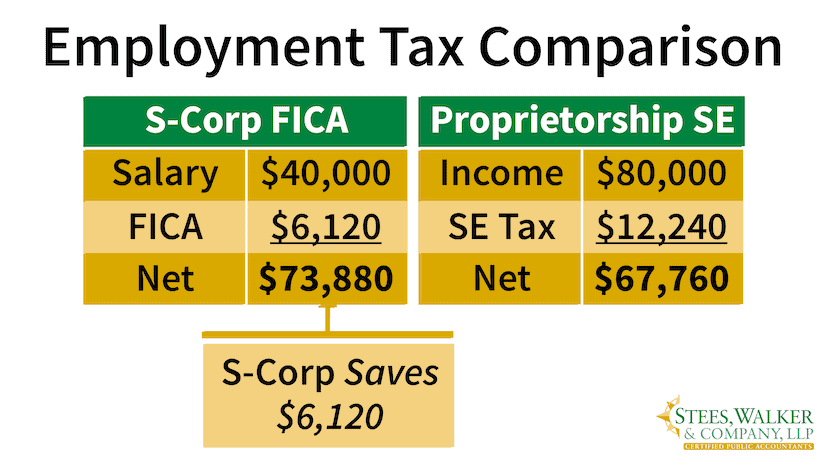

Suppose your profit at the end of the year is $80,000. You’ll pay income tax on that amount at your regular rate, whatever that is.

You’ll also owe about $12,240 in self-employment tax (15.3 percent of $80,000). On the other hand, if you had earned that $80,000 working a regular job, you would pay only half that amount — $6,120 Your employer would pay the other half. As a sole proprietor, you do get to deduct half of your self-employment tax from your income, which takes a little of the sting out of self-employment tax. In this example, that would drop your taxable income from $80,000 to $72,000.

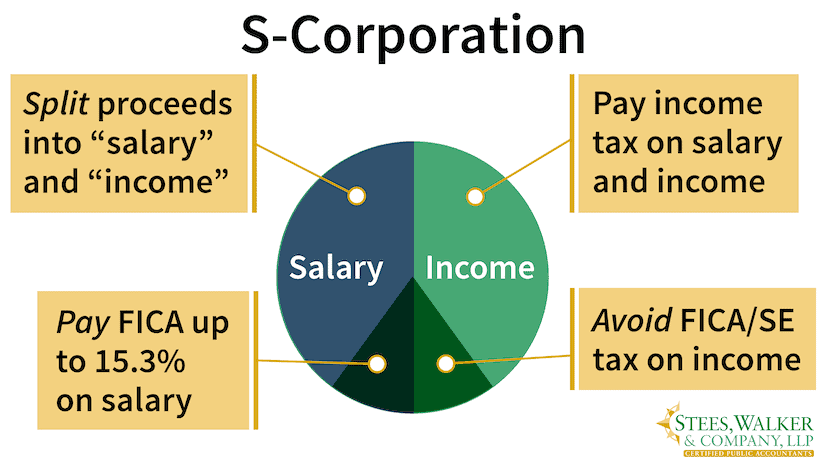

To reduce your self-employment tax significantly more, you can structure your business as an S corporation and take half the profit from that business as salary (subject to self-employment tax) and the other half in distributions (not subject to self-employment tax). You’re required to pay self-employment tax on the salary but not on the distributions, so with an S corporation, instead of paying self-employment tax on $80,000, you pay that 15.3 percent on only $40,000, slashing your self-employment tax in half. Instead of paying $12,240, you pay $6,120.

As you’ll see below, it’s like giving yourself a tax credit of $6,120!

Now, suppose you invest $6,000 of that $6,120 in a tax-deferred individual retirement account (IRA). That drops your taxable income from $80,000 to $74,000 for an additional savings.

Note that you must pay yourself a “reasonable compensation” from the S corporation — whatever amount you would have to pay an employee to do the work for you. If you pay yourself nothing, or merely a token amount, and take the remaining profit out of the business as a distribution, you’re going to increase your chances of being audited. If you are audited, the IRS may recharacterize up to 100 percent of your income as salary and hit you with some very hefty taxes, interest, and penalties.

So, don’t get greedy!

According to IRS data, the average S corporation pays out about 40 percent of its profits in salary and 60 percent in distributions. We can help you calculate a “reasonable compensation” for your business.

What’s the Catch?

The big drawback of using an S corporation to reduce your self-employment tax is that it also reduces the declared wages on which your future Social Security payments will be based, meaning your future Social Security payments could be cut in half.

The key to overcoming this drawback is to invest the amount you save in self-employment tax toward your retirement. If you invest that money wisely, you have the potential of generating your own retirement payouts that are more than what you would receive in the form of Social Security payments.

Another drawback involves the hassle of creating and maintaining partnership or corporation status. With an S corporation, for example, you’re required to set up a board of directors, file annual reports, conduct shareholder meetings, keep records of your meeting minutes, and jump through other hoops to maintain your corporate status. You can outsource this busywork to a lawyer or legal service, but that adds to the costs.

In addition, paying yourself a salary from the S corporation requires that you do payroll, complete with calculating withholdings from your payroll checks. We can help with that, but again, it’s an added cost.

Can’t I Just File as an LLC?

No. An LLC is a legal entity, not a tax entity. If you operate as a single-member LLC that is not also a partnership, S corporation, or C corporation, the default tax entity is sole-proprietor. If you’re operating as a single-member LLC and you’re reporting your business profit on Schedule C, your business is being taxed as a sole proprietorship, which has three major disadvantages:

- Reporting business profits as a sole proprietor is the most expensive way to file your taxes, even if you operate the business as an LLC.

- As a sole proprietor, if your business earns more than $100,000 in gross income, you’re five times more likely to be audited by the IRS, regardless of whether you operate the business as an LLC.

- As a sole proprietor, you’re responsible for paying self-employment taxes on 100 percent of your business profits. Operating as an LLC provides no tax benefit in this area.

The takeaway here is that no single business entity is best for every small-business and every small-business owner. You may be better off operating your business as a partnership, an S corporation, or a C corporation, and that can change as your business grows. Or the best option may be a combination of business entities; for example, an LLC operating as an S corporation.

Here at Stees, Walker, and Company, we can help you identify the most beneficial business entity(ies) for your business. The Tax Cuts and Jobs Act of 2017 makes this choice of business entity even more important by providing a new deduction for “qualified business income,” which just happens to be the subject of next week’s post.

– – – – – – – – –

Disclaimer: The information in this blog post about selecting a business entity is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter, or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment