Over the past 40 years or so, large and small businesses alike have been using Form 1099-MISC (short for miscellaneous income) to report payments of $600 or more in a calendar year to independent contractors, freelancers, sole-proprietors, and other self-employed individuals. Prior to that, these same businesses used Form 1099-NEC (short for non-employee compensation) for that purpose.

Well, the IRS (Internal Revenue Service) is turning the clock back to the 1980s with the return of Form 1099-NEC.

We can honestly say we didn’t see this one coming. In fact, we thought that the return of Form 1099-NEC was about as likely as, say, a third Bill and Ted movie. Well, we were wrong on both counts. And the funny coincidence is that the return of the 1099-NEC and the release of the third movie (Bill and Ted Face the Music) have both occurred in the same year — 2020, as if this year wasn’t already peculiar enough.

Taking a Closer Look at Form 1099 MISC

Before we look at what changed in 2020 regarding Form 1099-MISC, let’s take a look at what we have all become accustomed to for nearly four decades. Since 1982, businesses that have paid non-employees for their work have issued them a Form 1099-MISC in lieu of a W-2 form (required to report employee compensation).

For the past 38 years, most businesses have been using the 1099-MISC form to report any payments to independent contractors, freelancers, sole-proprietors, and other self-employed individuals who met any of the following three criteria:

- Received at least $10 in royalties or broker payments in lieu of dividends or tax-exempt interest

- Received at least $600 in:

- Rents

- Prizes and awards

- Other income payments

- Medical and health care payments

- Crop insurance proceeds

- Cash payments for fish (or other aquatic life) you purchase from anyone engaged in the trade or business of catching fish

- Generally, the cash paid from a notional principal contract to an individual, partnership, or estate

- Payments to an attorney

- Any fishing boat proceeds

- Someone who sells at least $5,000 in the aggregate of consumer products to a buyer for resale anywhere other than a permanent retail establishment is required to report the sale by checking item 9 on Form 1099-MISC.

What Changed?

The year 2020 is shaping up to be one of the most complex tax years on record. Large and small businesses, along with independent contractors, are already struggling to understand the tax implications of Paycheck Protection Program (PPP) loans and the Coronavirus Aid, Relief, and Economic Security (CARES) Act. To add to the complexity and confusion, the IRS is moving forward with its plan to resurrect Form 1099-NEC.

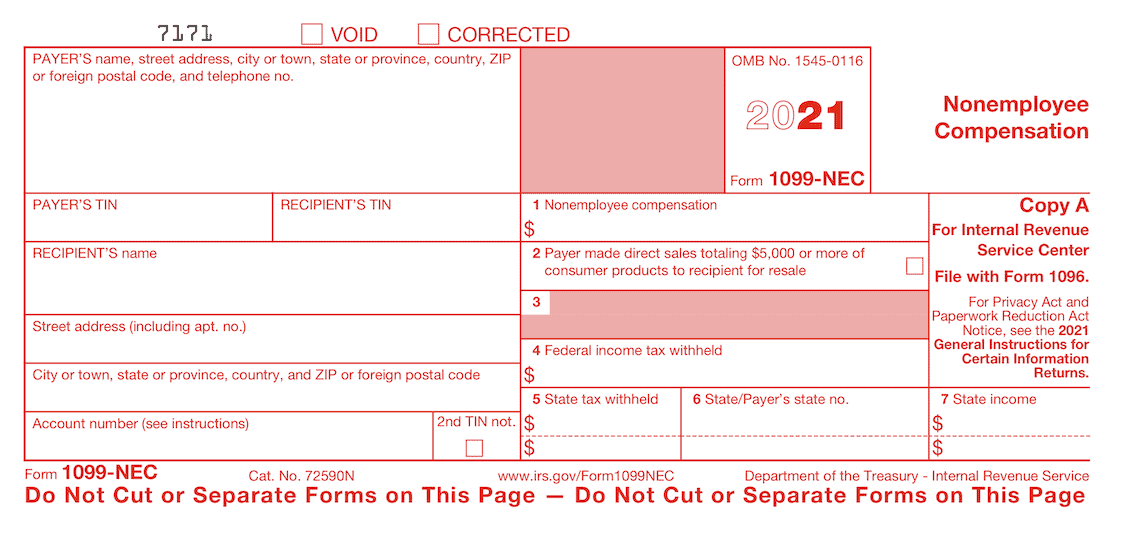

Prior to 1982, the income items listed above were reported using two forms — the 1099-NEC to report non-employee compensation, and 1099-MISC for everything else, such as rents, royalties, and prizes and awards. In 1982, the IRS decided to lump all these payments together for simplicity. Starting in tax year 2020, it is separating them out again.

Now, Form 1099-NEC is to be used to report only income and any federal and state withholding for non-employee compensation and/or nonqualified deferred compensation, payments for legal services, and any amount of cash received for fish (or other aquatic life) for those in the trade or business of catching fish. All other payments to service providers continues to be reported on Form 1099-MISC.

Understanding Why the IRS is Implementing This Change

The IRS is reinstating the 1099-NEC to solve a problem with due dates that was causing confusion for IRS software, systems, and personnel, as well as for taxpayers and employers.

In 2015, the Protecting Americans from Tax Hikes (PATH) Act required non-employee compensation to be reported to the IRS on Form 1099-MISC by Jan. 31. Meanwhile, the due date for filing Form 1099-MISC without non-employee compensation was set to Feb. 28 (or March 31 if filing electronically). So, the IRS had two due dates for the same form containing two different types of information.

The solution was to bring back Form 1099-NEC so there could be separate due dates for Forms 1099-NEC and 1099-MISC.

What to File

Businesses (including sole-proprietorships and nonprofit organizations) that used Form 1099-MISC to report non-employee compensation in the past are now required to use Form 1099-NEC to report any total payment of $600 or more during the tax year to a non-employee for any of the following:

- Services of an independent contractor (including parts and materials)

- Directors’ fees

- Legal services

- Fish purchases, for those in the trade or businesses of purchasing fish (or other aquatic life) for resale

Businesses are to continue using Form 1099-MISC to report all other payments, such as rents, royalties, and prizes/awards.

IMPORTANT: If your business files any Forms 1099-NEC or 1099-MISC, you must also use Form 1096 with the IRS to summarize the information you reported on those forms.

Filing Deadlines

The filing deadlines for Forms 1099-NEC and 1099-MISC, along with their corresponding Form 1096, differ:

- For 2021, Forms 1099-NEC and their corresponding Form 1096 must be filed by Feb. 1, 2021 (because Jan. 31, 2021 falls on Sunday)

- For 2021, Form 1099-MISC and their corresponding Form 1096 must be filed by March 1, 2021, if filed by paper, or March 31, 2021, if filed electronically (because Feb. 28, 2021, falls on a Sunday).

Implementing the Change

Switching from Form 1099-MISC to Form 1099-NEC to report non-employee compensation is straightforward, but implementation could be challenging. Here at Stees, Walker & Company, LLP, we recommend the following steps to ensure that you’re prepared to accommodate this change in your business by 2021:

- If you use accounting software, contact your software rep to ensure that the software will have the appropriate identifiers in place to pull the payments that require Form 1099-NEC.

- If you’re an independent contractor or freelancer, or sole-proprietor, let your clients know that they’ll need to issue you a Form 1099-NEC instead of the Form 1099-MISC for tax year 2020. You can use the same letter later in this post to notify your clients.

- If your company has a client accounting services department, consider performing a process and procedures scrub to ensure that reporting non-employee compensation versus other income is properly tracked for workflow and due dates. You may need to make the following adjustments:

- Educate staff on the new reporting requirements

- Contact your operations officer to be sure procedures are updated

- Update the workflow software to account for new tasks and due dates

By being proactive in implementing these changes and resolving any problems that arise, you’ll be well positioned for a smooth transition from 2020 to 2021.

Whether you plan to issue any Forms 1099-NEC or 1099-MISC for the tax year 2020 or later, and you have any questions or concerns, please contact us here at Stees, Walker & Company, LLP for assistance.

In the meantime, the sample letter we referenced above appears below.

Sample Letter for Independent Contractors to Send to their Clients

Dear ________,

Greetings! The reason I’m writing is to let you know (if you don’t know already) that the IRS is changing its reporting requirements for payments to independent contractors like me.

Starting with the current tax year (2020), instead of using a 1099-MISC, you will be using the new Form 1099-NEC (short for non-employee compensation) if you paid me more than $600 this year.

Form 1099-NEC is required to report total payments of at least $600 to attorneys, independent contractors, or directors, among others. You will continue to use Form 1099-MISC to report other payments such as rents, royalties, and prizes. Recipients like me are supposed to receive their 1099-NECs or 1099-MISCs by Feb. 1, 2021.

Filing deadlines for the IRS are Feb. 1, 2021, for Forms 1099-NEC (paper or electronic) and March 1, 2021, for Forms 1099-MISC (if filing by paper) or March 31, 2021, (if filing electronically).

Wishing you a productive, profitable, and Happy New Year!

Sincerely,

– – – – – – – – –

Disclaimer: The information in this blog post about IRS Form 1099-NEC is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment