Some of the most powerful tools for cutting taxes are tax-deferred retirement accounts, which enable you to invest money tax-free now, then pay taxes on it when you withdraw it in your retirement years. As a small-business owner, you can take advantage of several different types of tax-deferred retirement accounts, including individual retirement accounts (IRA), a simplified employee pension (SEP), a Savings Incentive Match Plan for Employees (SIMPLE) IRA, 401(k), Defined Benefit Plans, and even the option of a hybrid plan. Roth IRAs and permanent life insurance plans are two more tools that can benefit you when planning for retirement.

Many people have one or more retirement accounts, which is great, but few have a retirement plan — a highly specific approach for using retirement accounts to maximize their tax savings and achieve their retirement goals. Without a properly crafted retirement plan in place, mistakes are more likely, such as choosing an account type with a contribution limit that’s too low, exposing yourself to high taxes when you retire, or paying too much in account/plan management fees.

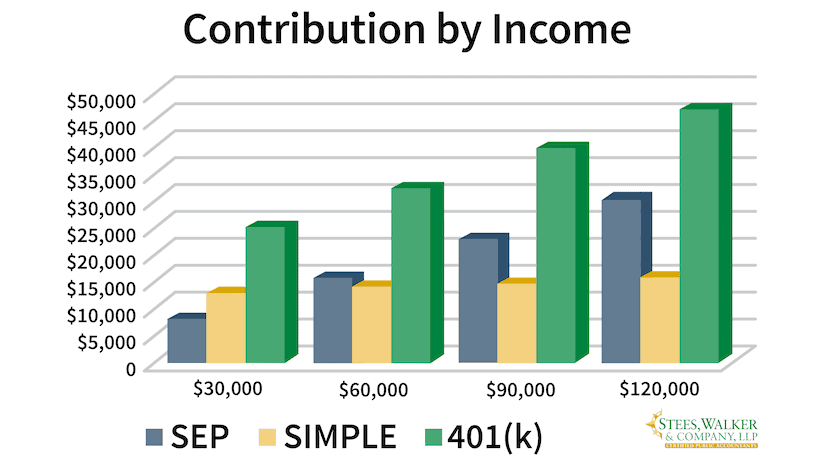

For example, depending on your income and the type of retirement account, your contribution limit varies considerably. If you earn $90,000, for example, you can contribute $16,200 to a SIMPLE IRA, or $22,500 to a simplified employee pension (SEP), or $42,000 to a 401(k). (Note: That’s before any catch-up contributions you can start making at the age of 50.) In some cases, plans can be combined to create even greater contribution potential.

But contribution limits aren’t the only thing you need to know. Which plan gives you the best combination of contribution limit, flexibility, liquidity, and cost? In addition, you need to consider that the decisions you make now can have long-term implications, possibly even limiting your future choices.

At Stees, Walker & Company, LLP we’re not here to make you a subject matter expert on retirement accounts. But we can help you decide if the account(s) you have are the right fit for you and your business and provide some guidance on how to use retirement accounts most effectively in the context of an overarching retirement plan.

We’ll assume for the purposes of this part in our 12-Part series on reducing your tax burden legally that you’ve already decided you want to contribute more to your retirement than the $6k you can contribute each year toward a traditional IRA. We’ll also limit the information we provide, at least over the first part of this blog post, to tax-deferred accounts, which involve claiming a deduction for your contributions now and then paying taxes on the money you withdraw during retirement.

Note: Toward the end of this post, we address other financial vehicles that may be advantageous to you in retirement, including Roth IRAs and permanent life insurance. But first, let’s cover the SEP (simplified employee pension).

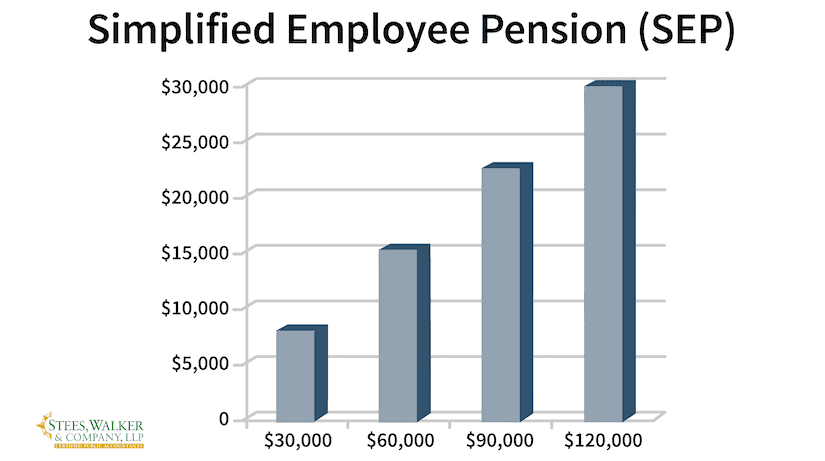

Understanding the Simplified Employee Pension (SEP)

The Simplified Employee Pension (SEP), which was authorized by Congress and is monitored by the IRS, is the easiest plan to set up.

The SEP is essentially a turbocharged IRA, and the rules governing it are pretty straightforward:

- If you’re self-employed, you can contribute up to 25 percent of your net self-employment income.

- If your business is incorporated and you’re salaried, you can contribute 25 percent of your salary (aka, your covered compensation).

- The maximum contribution for any one employee in 2020 is $57,000.

- If you have employees, you must contribute for them also — generally the same percentage for your employees as you contribute for yourself. Note that if your income is much higher than your employees, you can use an “integrated” formula to make additional contributions for higher income earners.

- The money goes directly into regular IRA accounts you set up for your employees and yourself. No annual administration or paperwork is required.

- SEP assets accumulate tax-deferred over time. You’ll pay tax on them at ordinary income rates when you withdraw them when you’re in retirement. Penalties apply for early withdrawals (before age 59 1⁄2) and for failing to take required minimum distributions (beginning at age 70 1⁄2).

The Simplified Employee Pension is easy to adopt, easy to maintain, and flexible. If no money is available to contribute, you simply do not contribute. Keep in mind however that the contribution is limited to a percentage of your covered compensation. For example, if you set up an S corporation to limit your self-employment tax (as explained in Part 3 of this series — Selecting a Business Entity), you’ll also limit your SEP contribution because it’s based on that lower salary amount.

Understanding the SIMPLE IRA

The next step up the retirement plan ladder is the SIMPLE IRA. If you’ve ever wondered what SIMPLE stands for, here it is: Savings Incentive Match PLan for Employees. See, wasn’t that simple?

The SIMPLE IRA is a ”supercharged” IRA that allows you to contribute more than the traditional IRA’s $6,000/year limit. Here are the rules for a SIMPLE IRA:

- You and your employees can defer and deduct 100 percent of your income up to $13,500.

- If you’re 50 or older you can make an extra $3,000 “catch up” contribution per year.

- You must match everyone’s deferral or make profit-sharing contributions. One option is to match employee contributions dollar-for-dollar up to 3 percent of their pay; you can reduce that 3 percent to as low as 1 percent for every two out of five years. The other option is to contribute 2 percent of each employee’s wages (up to $280,000), regardless of whether they choose to

- The money goes straight into employee Individual Retirement Accounts. While you’re allowed to designate a single financial institution to hold the money, if you choose you can allow your employees to choose where to hold their accounts.

- SIMPLE plans have no annual administration fee or set-up charge . Since you’re simply establishing special IRAs for your employees, you’re thought of as having established a qualified plan trust to hold the assets as you would with a 401(k) or defined benefit plan.

- SIMPLE assets accumulate tax-deferred over time. That means you’ll pay tax at ordinary income rates when you withdraw funds in retirement. Penalties apply for any early withdrawals (before age 59 1⁄2) and for failing to take required minimum distributions (beginning at age 70 1⁄2).

The SIMPLE IRA may be best for part-time or hobby businesses earning less than $54,000 per year, because the flat $13,500 contribution is higher than the 25 percent SEP contribution for incomes up to $54,000. And it may be best for lower-paid employees. The maximum contribution is below the $19,500 limit for a 401(k), but you have to stop to consider how many of your employees will actually contribute that maximum amount anyway.

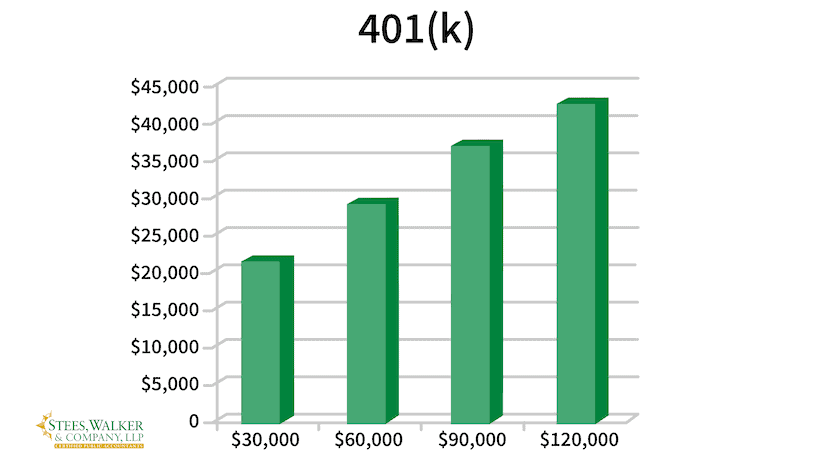

Understanding the 401(k)

Moving on, the next step up the retirement plan ladder is the 401(k).

Most people think of 401(k)s as retirement plans for bigger businesses, but you can set up a 401(k) for any size business. You can even set up what’s called a “solo” or “individual” 401(k) just for yourself.

If you’re unfamiliar with the history of the 401(k), it’s rather fascinating. As described in Helaine Olen’s national best seller, Pound Foolish: Exposing the Dark Side of the Personal Finance Industry, in the early 1970s, a group of high-earning executives from The Eastman Kodak Company approached members of Congress to allow a part of their salary to be invested in the stock market and thus be exempt from income taxes. According to Olen, this eventually resulted in section 401(k) being inserted in the then-current taxation regulations that allowed what the Kodak executives had lobbied for to be done.

As a result, the 401(k) — which refers to subsection 401(k) of the Internal Revenue Code — is a true “qualified” plan. This means you’ll set up a trust, adopt a written plan agreement, and choose a trustee. And here’s the great thing to know: the 401(k) lets you contribute far more money, and it is far more flexible than either the SEP or the SIMPLE. Here’s how it works:

- You and your employees can “defer” and deduct 100 percent of your income up to $19,500 for 2020. If you’re 50 or older, you can make an extra $6,000 “catch up” contribution.

- You can choose to match contributions or make profit-sharing ”contributions up to 25% percent of everyone’s pay. (If you operate as an S corporation, you can contribute up to 25 percent of your salary, but not any pass-through distributions you receive.) That’s the same percentage you can save in your SEP — on top of the $19,500 deferral.

- The maximum contribution for 2020 is $57,000 per person, plus any “catch up” contributions.

- You can offer yourself and your employees, loans, hardship withdrawals, and all the benefits large corporations offer their employees.

- You can use cross-testing to skew profit-sharing contributions to favored employees. For example, age-weighted plans allow you to allocate more to older employees; integrated and super-integrate” plans allow you to allocate more to higher-earning employees (on the theory that they receive little to no benefit from Social Security for their income above the Social Security wage base); and rate group plans allow you to divide employees into groups (such as administrators, managers,, and sales team members) and make different contributions for each group.

- 401(k) assets accumulate tax-deferred over time. That means you’ll pay tax at ordinary income rates when you withdraw them in retirement. Penalties apply for any early withdrawals (before age 59 1⁄2) and for failing to take required minimum distributions (beginning at age 70 1⁄2).

What’s the downside to the 401(k)? Well, 401(k)s are true “qualified” plans, which means more administration is required than simplified employee pensions (SEPs) or SIMPLE IRAs. As a result, you’ll have to file IRS Form 5500 (the Annual Report/Report of Employee benefit Plan form) reporting contributions and assets every year. Also, there are important anti-discrimination and other rules to keep you from shorting your employees while you pad your own account.

Another big downside of 401(k)s is that the U.S. Department of Labor recently targeted hidden fees in 401(k)s and mandated that retirement account sales reps follow a fiduciary standard, not the less stringent suitability standard. As a result, many financial services companies are leaving the 401(k) market. By one estimate, the mandated change will impact nearly $3 trillion of retirement assets and $19 billion of revenue in the financial services industry. If you control your business’s 401(k), this change can impact you, too, possibly drawing increased scrutiny from the Department of Labor.

However, if the 401(k) really does make sense for you and your business, these three alternatives might make the administration of the plan somewhat easier:

- A “SIMPLE” 401(k) avoids nondiscrimination and top-heavy rules in exchange for guaranteed employer contributions. You and your employees can defer 25 percent of covered compensation up to the SIMPLE plan contribution limits. Your business must contribute 2 percent of covered compensation or match contributions up to 3 percent of covered compensation. This works if you want a true 401(k), but you’re afraid your employees won’t contribute enough to let you make meaningful deferrals. You can also convert an existing 401(k) to a SIMPLE 401(k).

- A “Safe Harbor” 401(k) avoids nondiscrimination (but not top-heavy) rules in exchange for bigger employee contributions. You and your employees can defer up to the regular 401(k) limit. You can either: 1) contribute 3 percent of covered compensation; or 2) match contributions dollar-for-dollar up to 3 percent of covered compensation and fifty-cents-on-the-dollar for contributions between 3 percent and 5 percent of covered compensation. You can even make extra profit-sharing contributions on top of the required contributions.

- If you operate your business entirely on your own with no employees other than your spouse, you can establish an “individual” 401(k) with much less red tape.

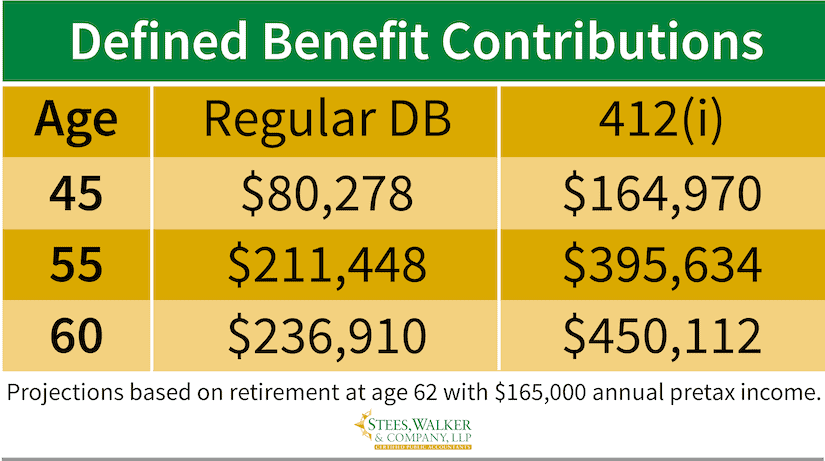

Understanding the Defined Benefit Plan

Now, if you really want to contribute more than the $57,000 limit for SEPs or 401(k)s, consider a defined benefit plan. This is your mother’s retirement plan — the traditional “pension plan” that so many U.S. employers have stopped offering because they simply can’t afford to maintain it anymore. However, it can still be a great choice for older, highly compensated business owners with few employees. For instance:

- Defined benefit plans let you guarantee up to $230,000 in annual income (2020 limit).

- You can contribute and deduct as much as you need to finance that benefit. You’ll calculate those contributions according to your age, your desired retirement age, your current income, and various actuarial factors that your tax planning and financial services advisory firm can help you with.

The biggest challenge with the defined benefit plan is the required annual contributions. That means, if your business doesn’t have the money, you still have to pay. However, you can combine a defined benefit plan with a 401(k) or SEP to give yourself a little more flexibility. Suppose you could contribute up to $100,000 to a defined benefit plan, but you’re not certain that you can commit to that much every year. In that case, you might be smart to set up a defined benefit plan with a $50,000 contribution, then pair it with 401(k) for another $50,000. If business is slow in a particular year, you can choose to skip the 401(k) that year.

Using Other Account Types in Your Retirement Plan

Now that we’ve covered the menu of traditional employer-sponsored retirement plans, let’s cover a potentially reasonable complication . Do you even need or want a traditional plan, or would you be better off with an alternative, perhaps even giving up the current tax break?

All of the plans we covered so far assume that you’re better off taking a tax deduction for contributions now, letting the assets grow tax-free over time, and then paying tax on withdrawals at ordinary income rates when you need them for retirement.

That’s a great approach if your tax rate is higher now than it will be in retirement. It puts more of your money to work for you right now, and you benefit later by paying less tax on withdrawals.

But that traditional pattern doesn’t always hold true. Say you’re young, just starting your career, and your income is low (and so is your tax rate). Maybe you’re repositioning yourself from one career or business to another, and your income is currently low. Maybe you think that tax rates in general will rise. (Today’s top marginal rate may seem high at 37 percent, but that’s actually low by historical standards.) Sometimes, contributing to a traditional retirement plan creates a ticking tax time bomb and actually costs you money over the long run.

You have two additional tools at your disposal when you’re planning for retirement — Roth IRAs and permanent life insurance policies.

Using Roth IRAs to Your Advantage

Roth IRAs turn the traditional defer-now-pay-later arrangement on its head. You invest after-tax dollars now and withdraw them later, generally tax-free, as long as they’ve aged at least five years.

Tax-free income sounds great, right? Well, contributions are limited to $6,000 per year ($7,000 if you’re 50 or older), and you cannot contribute at all if your income is over $139,000 (single filers) or $206,000 (joint filers). If your income is above those limits, you can still fund a Roth by contributing the maximum to a nondeductible traditional IRA, then immediately converting it to a Roth.

If your business sponsors a 401(k), you can choose to designate your salary deferrals up to $19,500 as Roth deferrals. You won’t receive any deduction today, but your future withdrawals will be tax-free. (Any employer contributions will continue to be treated as deductible now and taxable later.)

If you have a simplified employee pension (SEP) , you can create a backdoor “Roth SEP” by making a deductible SEP contribution, then immediately converting it to a Roth. Roth conversions are a subject for another post; we just want you to be aware that the possibility exists. (Note: You can do the same with a Savings Incentive Match Plan for Employees (SIMPLE), but you have to wait at least two years from the time you contribute the money to convert it to a Roth.)

Leveraging the Power of Permanent Life Insurance Policies

Permanent life insurance policies that have a cash value can offer several significant tax breaks for supplemental retirement savings. You don’t get to claim a deduction for the premiums you pay into the contract, but the policy’s cash value grows tax deferred. And you can take cash from your policy tax-free by withdrawing your original premiums and then borrowing against remaining cash values. You’ll pay (nondeductible) interest on your loan but earn it back on your cash value. Many insurers offer “wash loan” provisions that let you borrow against your policy with little or no out-of-pocket costs.

Note: These advantages aren’t completely unlimited. If you place too much cash into the policy in the first seven (7) years, it’s considered a “modified endowment contract” and all withdrawals are taxed as ordinary income until you exhaust your inside buildup.

Insurers offer three main types of cash-value policies with three different investment profiles to suit different investors. The key is finding a policy that matches your investment temperament:

- “Whole life” resembles a bank CD in a tax-advantaged wrapper, with required annual premiums and strong guarantees. Remember when we said the defined benefit pension was your father’s pension plan? Well, this is your mother’s life insurance.

- “Universal life” generally resembles a bond fund in a tax-advantaged wrapper, with flexible premiums but weaker guarantees. Some insurers also offer “indexed universal life,” which lets you profit from equity markets but gives you a guaranteed return even when those markets are down.

- “Variable life” lets you invest cash values in a series of “subaccounts” resembling mutual funds in a tax-deferred wrapper. You can choose “variable whole life” with required premiums and stronger guarantees, or “variable universal life” contracts with flexible premiums and weaker guarantees.

Again, we’re not trying to make you an expert on retirement accounts and other financial tools for minimizing your taxes and maximizing your return at retirement. Our objective is to open your eyes to the wide variety of accounts and other options so that you have a general idea of what’s possible when you discuss retirement with your accountant or financial planner. We also want to keep you from falling into the common trap of assuming that deferring today’s income is always best.

Regardless of whether you already have one or more retirement accounts, we urge you to meet with your accountant or financial planner to develop a retirement plan and discuss what you already have in place (if anything). Making a few adjustments could save you money now while ensuring a more secure and comfortable future.

Next week, we continue our series by explaining how you can reduce your taxes by paying wages to family members who work for your business. And then maybe they can start saving for retirement, too!

– – – – – – – –

Disclaimer: The information in this blog post about leveraging the tax savings power of retirement accounts, is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment