If you own real estate, or you’re interested in investing in real estate as a strategy for building or increasing your net worth, then you need to know about cost segregation.

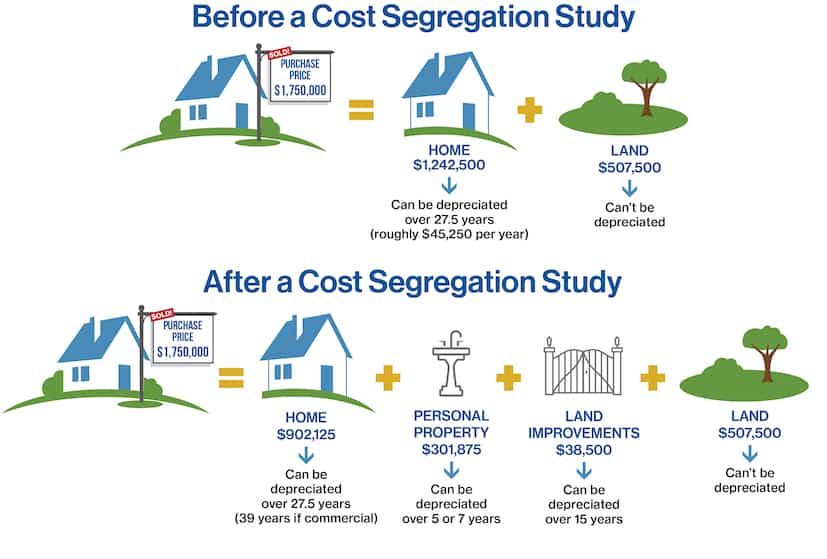

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

This reallocation can provide significant tax benefits because shorter-lived assets are eligible for accelerated depreciation.

Depreciation 101: Depreciation is an accounting technique that distributes the cost of tangible assets such as real estate over their useful lifespan. It reflects the portion of an asset’s value that’s been utilized, allowing you to gradually pay for and generate revenue from an asset over a specified period of time.

When a property is built or purchased, the costs of the property (such as construction costs or the purchase price and cost of improvements) are typically allocated to the building and land as long-term assets. However, many of the items within a property (such as carpeting, lighting fixtures, and appliances) have a shorter useful life and can be classified as personal property. By identifying these shorter-lived assets and reclassifying them as personal property, the costs associated with them can be depreciated over a shorter period, resulting in a larger tax deduction in the early years of ownership.

Starting With a Cost Segregation Study

To add cost segregation to your tax planning approach, start by ordering a cost segregation study from a reputable firm. Here at SWC, we work with several of these firms and can recommend the right one for your particular circumstances and objectives.

When you engage a firm in a cost segregation study, a cost segregation specialist identifies and reclassifies the costs of your property, typically by examining the property and its invoices, blueprints, and other documentation. The study then allocates property costs to real property or personal property. Findings from the study can then be used by your tax planning firm — in this case, SWC — to calculate a one-time catch- adjustment. That’s because the IRS allows the depreciation deductions from prior years to be recomputed and deducted in the current tax year. As a result, the adjustment doesn’t require any prior year tax returns to be amended.

Pro Tip: A cost segregation study can be performed on both new construction and existing properties, and it can continue to provide tax savings each year the property is owned.

Differentiating Personal Property from Real Property

Cost segregation involves recategorizing real property as personal property, which begs the question — what’s the difference?

Real property consists of land, buildings, and permanent structures, such as the following:

- Walls

- Roof

- Foundation

- Mechanicals that cannot be easily moved or removed from the property such as HVAC systems, plumbing, and electrical service distribution systems

These items all have a long useful life and are generally depreciated over a long time.

Personal property has a shorter useful life and can be depreciated over a shorter period of time. In the context of real estate, the IRS generally allows the following to be categorized as personal property:

- Flooring such as carpet

- Window treatments — curtains, blinds, and so on

- Lighting fixtures and electrical systems

- Appliances and equipment

- Furniture

- Bathroom and kitchen fixtures

- Other interior items

To be reclassified as personal property, the IRS says an asset must meet the following criteria:

- Have a useful life of less than 27.5 years.

- Be able to be separated from the real property without causing significant damage.

- Not be a structural component of the building.

- Be used for the production of income.

- Be able to be moved.

- Be depreciable.

The IRS also requires specific documentation to support the reclassification of assets as personal property. As a result, a cost segregation study must be conducted by a qualified professional and must include the detailed information about the property and the assets being reclassified, as previously covered in this post.

Warning: The IRS has increased its focus on cost segregation studies in recent years and may perform an audit to verify the validity of the study and the reclassification of assets. Therefore, it’s important that the study be performed correctly and that you have all the necessary documentation readily available in case of an audit.

Recognizing the Potential Benefits of Cost Segregation

Overall, cost segregation can be a powerful tool for savvy real estate investors and property owners to maximize the tax benefits of their property investments:

- Cost segregation can be especially beneficial if you recently built or purchased a property, because the additional deductions can significantly reduce your tax liability in the early years of ownership.

- You can also use cost segregation to enhance a property’s cash flow by accelerating the depreciation deductions, which reduces your taxable income.

Recognizing the Risks of Cost Segregation

While cost segregation can provide significant tax benefits for property owners and investors, beware of the following potential risks:

- The IRS may challenge the reclassification of assets. That’s because the IRS has strict guidelines for what can be considered personal property. If your cost segregation study is not conducted correctly, the IRS may disallow some or all of the additional deductions you claim.

- As the property owner, you may be required to remove or dispose of certain personal property assets at the end of their useful life, which can be costly and disruptive.

- Cost segregation can increase the complexity of your tax return, making it more difficult to file and increasing the chances of errors.

- The cost segregation study itself can be costly. Be sure to weigh the potential benefits against the costs.

Keep in mind: Cost segregation alone doesn’t guarantee tax savings, especially over the long haul. We encourage you to consider it as a small part of a larger tax-savings and wealth-building strategy.

Overall, while cost segregation can be a powerful tool for real estate investors and property owners to maximize the tax benefits of their investments, you need to be aware of the risks and consult with a tax professional before adding cost segregation to your tax-saving and wealth-building strategy.

If you think that you may benefit from cost segregation, contact us at SWC and schedule a consultation. We can help you decide if it’s right for you. If it is, we can provide guidance on how to proceed.

——-

About the Author: Jennifer Shelton, CPA, is an accountant at SWC — a San Diego, Calif.-based tax planning and financial strategy advisory firm for small-business owners, real estate investors, and high-net-worth individuals. A graduate of Kansas State University and a member of the Kansas Society of Certified Public Accountants (KSCPA) and the American Institute of Certified Public Accountants (AICPA), Jennifer has more than 15 years of experience in public accounting with a background in taxation and accounting.

Disclaimer: The information in this blog post about cost segregation studies is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at SWC (Stees, Walker & Company, LLP), nor is the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment