If you’re thinking about selling an investment property, the first question you should ask before anything else: How much of my profit will go to taxes?

For real estate investors, entrepreneurs, and high-net-worth individuals like the ones we work with here at SWC, the answer to that questions can be “tons!” That is, unless you know how to work the system. A like-kind exchange — also known as a 1031 exchange — enables you to sell one investment property and reinvest the proceeds into another, all while deferring capital gains taxes. It’s a savvy move, but only if you follow the rules.

In this post, we provide a clear breakdown of how like-kind exchanges work, what rules you need to follow, and how to make the most of this powerful tax-deferral strategy.

Here’s what you need to know.

Understanding the 1031 Exchange

A 1031, also known as a like-kind exchange, involves exchanging real estate used solely for business or held as an investment for other business or investment property that is the same type. For example, you may sell a rental property and buy a different rental property.

Generally, when you make a like-kind exchange, you’re not required to recognize a gain or loss under Internal Revenue Code Section 1031 (there’s where the moniker “1031 exchange” comes from.) However, if as part of the exchange, you also receive other (not like-kind) property or money, you must recognize that gain to the extent of the other property and/or money received. Under no circumstances can you recognize a loss.

Deploying a1031 exchange is a powerful strategy for real estate investors to postpone paying capital gains taxes on the sale of their investment properties. By selling one investment property and reinvesting the proceeds in another investment property of equal or greater value, you can defer capital gains and depreciation-recapture taxes. Better yet, by continuing to defer capital gains through successive like-kind exchanges, you may eventually qualify for a basis step-up, which can effectively eliminate the deferred taxes altogether!

Basis Step-Up? A basis step-up is an adjustment of the cost basis of an asset to its fair market value at the time of an owner’s death. If the cost basis of the investment property is equal to or greater than that for which the property ultimately sells, the profit from the sale is zero or negative, meaning no capital gains tax is owed.

A Sample Transaction

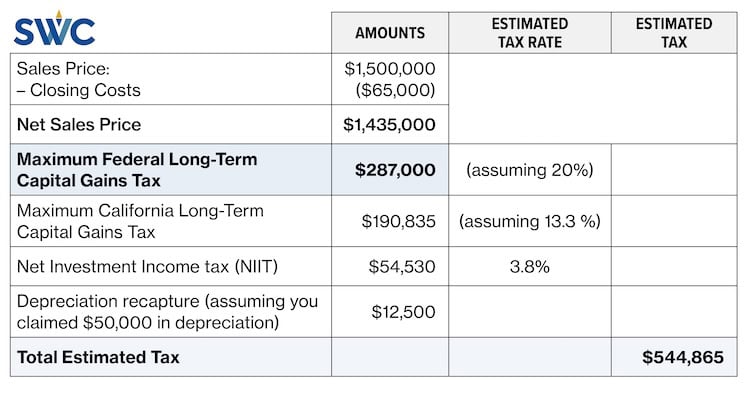

Capital gains taxes can be as high as 42.1 percent depending on your income, filing status, and state. If you’re a client of ours, we can provide a precise estimate. If you’re not one of our clients, we encourage you to consult your CPA to obtain an estimate based specifically on your unique situation. Before selling an investment property or a property you use exclusively for business purposes, you should always know how much you stand to lose in taxes.

Let’s look at how much money a like-kind / 1031 exchange could allow you to defer in taxes for the sale of a $1.5 million investment property in California:

Note that we simplified this example by excluding items such as the adjustable basis (purchase price + cost of improvements – depreciation claimed) and any mortgage payoff. Later in this post, we include these items in our example calculations.

Following the Rules for 1031 / Like-Kind Exchanges

To ensure that a real estate transaction qualifies as a like-kind exchange, you need to follow the IRS rules that govern these types of exchanges. Those rules include the following:

- Business or investment use only: To qualify as a like-kind exchange, all properties involved in the transaction must be used for business or investment purposes. Personal-use properties, such as primary residences or vacation homes, don’t qualify.

- Like-kind property only: You can exchange investment or commercial property for investment or commercial property. For example, you can exchange an apartment building or a rental property for commercial real estate. “Like kind” refers more to the purpose of the property (investment and business use as opposed to a personal residence or vacation property) and not to its condition.

- Must exchange a property of equal or greater value: To qualify for a full tax deferral, you must trade up or break even in both property value and equity. If you trade down in either value or equity, proceeds from the sale, whether cashed out or not, may be subject to capital gains tax. See the next section, “Performing the Napkin Test,” for details. If the replacement property has less debt than the relinquished one, the difference (called the “boot”) is taxable.

- Same taxpayer must be on both titles: The same taxpayer must be on title for both the sold and the purchased property with the exception of properties held in a Delaware Statutory Trust (DST) — a legal entity created as a trust that permits a very flexible approach to the design and operation of the entity. While the DST itself holds title to the property, the investor’s beneficial ownership in the DST must match the titling of their sold property.

- The 45-day identification rule: You have 45 days from the day of selling a property (Day 0) to identify potential replacement properties. See the later section, “Meeting the 45-Days-to-Identify Requirement,” for details.

- The 180-day exchange period rule: You must close on the purchase of the replacement property within 180 days of selling the original property.

- No direct receipt of funds: Investors are not permitted to have direct access to funds from the property sale. All funds must flow through a third-party intermediary — an escrow account.

- Investment holdings only: Fix-and-flip properties do not qualify for like-kind exchanges. To comply with this rule, we advise holding a property for at least a year, preferably for at least two years.

- Reporting requirements: The exchange must be reported on IRS Form 8824 and filed with your tax return.

Performing the Napkin Test

The ultimate goal of a like-kind exchange is to fully defer your capital gains tax. In some situations, however, you can partially defer this tax. For example, if you exchange a more expensive property for a less expensive one, you can defer only the portion of the proceeds invested in the new property. You cannot defer capital gains on the net proceeds you receive from the transaction.

To determine whether the capital gains from a like-kind exchange can be fully deferred, conduct the Napkin Test. This is a simple back-of-the-envelope calculation (see below) to determine whether you’ll be able to fully defer capital gains resulting from the exchange.

Here’s how to perform that Napkin Test:

- Determine the sale price of the relinquished property.

- Subtract the selling costs for the relinquished property (commissions, escrow, title fees, closing costs).

- Subtract the mortgage or debt payoff for the relinquished property. This gives you the net equity or cash proceeds from the sale.

- Determine the replacement property’s purchase price.

- Determine the down payment and loan amount on the new property.

- Compare the numbers for the relinquished and replacement properties to ensure that you’re not receiving any proceeds from the exchange. To have your capital gains tax fully deferred, you must be able to answer Yes to the following three questions:

- Did you pay more for the replacement property than the sale of the relinquished property?

- Did you reinvest all equity you had in the relinquished property?

- Is the debt on the replacement property greater than that of the relinquished property, or did you add cash to address any difference? To fully defer taxes when selling property, you must replace any paid-off debt in the new purchase using new debt, outside cash, or both.

- Determine if there’s a boot (taxable amount). If you cashed out any proceeds or reduced your loan amount (debt), that amount is considered a capital gain and is subject to capital gains tax.

Here’s an example of a Napkin Test:

- Relinquished property sold for $800,000 minus selling costs of $50,000 = $750,000. You pay off the mortgage of $300,000, leaving $450,000 in equity (cash proceeds).

- You plan to buy a replacement property for $900,000, reinvesting the $450,000 and taking out a $450,000 loan.

- According to the napkin test, you can answer Yes to the three key questions:

- You bought a property of greater value than the one you sold.

- You reinvested all the cash.

- You increased your debt from $300,000 (the mortgage balance on the relinquished property you sold) to $450,000 (the mortgage on the replacement property you purchased).

Meeting the 45-Days-to-Identify Requirement

Identifying like-kind properties within the 45-day window and then closing on the property within 180 days may be the most challenging requirements to meet. These deadlines can become even tighter if you find yourself dealing with market volatility, limited inventory, and difficult sellers. Problems with inspections, insurance, financing, and other associated activities can also complicate the process and slow progress.

Fortunately, the Internal Revenue Service (IRS) offers three different approaches (“rules”) for identifying like-kind properties (all properties must be located in the U.S.):

- The Three-Property Rule: You may identify up to three properties regardless of value and purchase one, two, or all three, as long as they were among the three you identified within the 45-day period.

- The 200 Percent Rule: You can identify more than three properties, if the total value of all the properties does not exceed 200 percent of the value of the relinquished property. For example, if you sold a property for $1 million, the combined fair market value (FMV) of all identified properties must be equal or less than $2 million.

- The 95 Percent Rule: If you exceed both the three-property and 200% limits, you can still maintain your eligibility for tax deferral if you acquire at least 95% of the total value of the replacement properties you initially identified.

Note: You are not obligated by the IRS to close on any of the properties you identified. However, only those properties that you identify as possible replacements and that you close on or within the 180-day period will qualify for a like-kind exchange.

Caution: If you fail to identify any properties within 45 days of selling, the property you’re selling will not qualify for a like-kind exchange, and all proceeds from the sale will be subject to capital gains tax.

Shifting Your Focus to the “Tax-on-Cash” Rate

When deciding between cashing out and doing a 1031 exchange, we recommend that you consider the tax-on-cash rate. The tax-on-cash rate is the effective tax rate you’ll pay on the equity (cash) you stand to receive if you sell an investment property and don’t do a like-kind exchange. Think of it as how much of your profit you stand to lose if you cash out.

To estimate your tax-on cash rate, take the following steps:

- Start with your gross sales price; for example, $1,000,000.

- Subtract your selling costs (commissions, escrow fees, title insurance, and so on); for example, $1,000,000 – $60,000 = $940,000. This is your net sales price.

- Subtract the mortgage payoff; for example, $940,000 – $400,000 = $540,000. This is your net equity or cash-in-hand you will receive from the sale.

- Calculate your adjusted basis (purchase price + cost of improvements – depreciation claimed); for example, $500,000 + $50,000 – $150,000 = $400,000.

- Calculate the total capital gain (net sales price – adjusted basis); for example, $940,000 – $400,000 = $540,000.

- Split the gain into two parts — the depreciation recapture portion ($150,000), which is taxed at 25 percent (for example) and the long-term capital gain portion ($540,000 – $150,000 = $390,000), which is taxed at a maximum of 20 percent.

- Apply the tax rates. For example, if you’re in the top tax brackets and you live in California:

Depreciation recapture at 25 percent is $150,000 x 0.25 = $37,500

Long-term capital gains at 20 percent is $390,000 x 0.20 = $78,000

NIIT at 3.8 percent is $540,000 x 0.038 = $20,520

California Tax at 13.3 percent is $540,000 x 0.133 = $71,820

Total Tax = $37,500 + $78,000 + $20,520 + $71,820 = $207,840 - Calculate your tax-on-cash rate, which is total tax divided by net equity:

$207,840 / $540,000 = 38.49 percent

That represents a significant portion of your profit going to the tax man. If your loan payoff were much lower (for example, $0) and your adjusted basis in the property were much higher (for example, $800,000 instead of $400,000), your tax-on-cash rate would be significantly lower. Suppose your adjusted basis were: $750,000 + $100,000 – $50,000 = $800,000

Your net equity or cash-in-hand after the sale would be $940,000, and your total capital gain would be $940,000 – $800,000 = $140,000.

Your taxes would look something like this:

- Depreciation recapture at 25 percent is $50,000 x 0.25 = $12,500

- Long-term capital gains at 20 percent is $90,000 x 0.20 = $18,000

- Net Investment Income Tax (NIIT) at 3.8 percent is $140,000 x 0.038 = $5,320

- California Tax at 13.3 percent is $140,000 x 0.133 = $18,620

- Total Tax = $12,500 + $18,000 + $5,320 + $18,620 = $54,440

In this scenario, your tax-on-cash rate would be: $54,440 / $940,000 = 5.8 percent

In this second scenario, cashing out makes a lot more sense.

Swap ’til You Drop

Since property appreciation leads to a buildup of capital gains taxes, you can defer these taxes by holding properties or making successive like-kind exchanges until you pass away. As long as the equity remains locked up in your investment or business real estate (you’re not cashing it out), you have no realized capital gains to tax.

One strategy that enables you to avoid these taxes altogether is commonly known as “swap ’til you drop.” With “swap ’til you drop,” you make successive like-kind exchanges until you die, at which point a basis step-upoccurs. The step-up adjusts the inherited asset’s cost basis to its fair market value at the owner’s death, potentially eliminating deferred taxes. In a community property state such as California, this step-up happens when the first spouse passes away (assuming they file jointly).

Here at SWC, we’re committed to helping our clients minimize their taxes while maximizing their net worth. We hate to see clients handing over a significant chunk of their hard-earned income or investment profits to the IRS and other taxing authorities.

If you own any investment or business properties, we strongly encourage you to understand the tax implications prior to selling any of them. Better yet, call us for a consultation at (858) 487-4580. We can help you through the entire process, including identifying, evaluating, and purchasing replacement properties to ensure that you comply with all the rules and regulations that apply to like-kind exchanges.

Don’t get blind-sided by a hefty tax bill just because you overlooked an important technicality.

Leave A Comment