Welcome to Our Blog

We’re a San Diego, Calif.-based boutique tax consulting firm focused on personalized tax and financial guidance to individuals and businesses. Here on our blog, you’ll find you’ll find news, insights, and observations from trusted sources in the world of tax planning and and financial guidance.

Introduction to Small Business Guide to Legally Reducing Your Tax Burden

Share This Post

If you’re like most small-business owners, you launched your business with a great idea for a product or service and a passion for delivering it to consumers or other businesses. You were probably unaware at the time of the heavy burden of managing your business, especially the complex financials, and especially those related to taxes. Like other business owners, you most likely started out not even knowing what you didn’t know, and that is perfectly understandable.

Surely you can’t be expected to know what you haven’t been taught, right? Unfortunately, the government (federal, state, and local) and their corresponding taxing authorities do expect you to know and follow the tax code. You have probably heard the edict, “Ignorance of the law is no excuse.” It’s true. In fact, what you don’t know about the tax code can cost you dearly in both penalties (for non-compliance) and overpayments (for not taking full advantage of your eligible tax breaks).

Many small-business owners are so afraid of the Internal Revenue Service (IRS) or so terrified of making a mistake that they end up paying more than their fair share in taxes — sometimes a lot more. And that makes those of us at Stees, Walker & Company, LLP want to scream. Why? Because we know that while making money is hard, keeping it is fairly easy, as long as you know what you’re doing and choose to work with a tax and financial planning firm like ours. And, for the most part, all that involves is knowing the tax code and keeping good records, both of which are our areas of expertise.

One way we can help without it costing you any more than your time is to provide free guidance and insight. As part of that focus, we’re launching an 11-part series here on our blog on how to reduce your tax burden legally. Starting next week and over the course of the next three months or so, we will be posting one part per week, each focusing in on a single technique for reducing taxes.

Here’s what we’ll cover in each part: Continue reading… Continue reading… Continue reading…

Distinguishing Employees from Independent Contractors Under California AB 5

Share This Post

Determining whether someone working for you is an employee or an independent contractor used to be easy. If the person worked for your business a certain number of hours per week, they were an employee with rights to benefits and overtime pay (when applicable). If the person didn’t meet those criteria, he or she was considered an independent contractor.

Back in 1987, the Internal Revenue Service (IRS) developed a list of 20 factors to examine in determining whether an employer-employee relationship exists. Based on case law and judicial rulings, the IRS determined that the degree of importance of each factor varied, depending on the occupation and context in which the services were performed.

But that all shifted last year here in the Golden State with the passing of California’s Assembly Bill 5 (AB5), which was signed into law by Gov. Gavin Newsom in September 2019 and went into effect on Jan. 1, 2020. That bill classifies most workers as employees, placing the burden of proof for classifying workers as independent contractors on the hiring entity (i.e., the small and medium size business, not-for-profit, or enterprise).

In essence, a worker is to be treated as an employee unless the business can prove otherwise. Another way to put it is that under AB5, it is California law — not businesses — that determines who is an independent contractor and who is not. It’s a fairly rigorous law, and both business owners and workers are understandably confused by it.

In this post, we set out to help you determine whether a person working or performing work for you is doing so as an employee or as an independent contractor under California’s AB5 law.

The ABC Test

The California bill replaces the common law test (the Borello test described later in this post) with the so-called ABC test to determine whether a worker is an employee or an independent contractor in California. And if you’re wondering why the test is named “ABC,” it’s because it features three parts — a Part A, a Part B, and a Part C.

For purposes of California employment laws, the test applies to those requiring minimum wage, overtime pay, unemployment insurance, workers’ compensation insurance, and paid family leave. As an aside, AB5 does not change how out-of-state workers are classified.

Under the rule established by AB5, hiring entities are now required to classify workers as employees unless the person in question meets all the following conditions of the ABC test: Continue reading… Continue reading… Continue reading…

Preparing for Your Complimentary Annual Mid-Year Meeting

Share This Post

Here at Stees, Walker & Company, LLP, we make it our responsibility to help our clients navigate the complexities of personal and business finances and maximize their tax savings, so they have more money to enjoy their lives and invest toward their financial futures. To fulfill this deeply rooted responsibility, every year at about this time, we offer our clients a complementary mid-year planning meeting. During each one-hour session, we discuss the client’s goals and any changes to their personal and/or business lives, identify ways to help them save money on taxes, answer any questions they have, and ensure that we are all working together toward the same financial goals.

Whether you’re a client of ours or another financial planning firm, you should engage in a midyear tax and financial planning session because the financial decisions and actions you take over the coming months can have a significant impact on your finances for years to come. However, very few people engage in such planning or they do so without professional guidance. As a result, we suspect that many people miss out on opportunities to reduce their taxes and have more money to invest toward their financial futures.

This year, we have a sense that more people might neglect their finances due to COVID-19. With the spring filing deadline postponed to July 15, many people are still focused on filing their 2019 tax returns. However, early preparation is key to taking advantage of future tax-saving opportunities, so we encourage you to meet with a qualified tax advisor or financial planner to explore opportunities to improve your finances.

In this post, we cover some of the recent changes in tax legislation and present a list of tax moves that you and your advisor may want to discuss.

Recent and Future Changes Likely to Impact Your Taxes

Several changes in tax legislation occurred near the end of 2019 and early in 2020 that are likely to provide tax-saving opportunities: Continue reading… Continue reading… Continue reading…

Update on How to Have Your Paycheck Protection Program Loan Forgiven

Share This Post

If you read our April 29 post, “How to Determine Loan Forgiveness Under the Paycheck Protection Program,” or if you’re an owner or manager of one of the nearly 4 million U.S. businesses that received a loan under the Paycheck Protection Program (PPP) — you’re probably starting to wonder how to go about having that loan converted to a grant and forgiven.

For the uninitiated, the PPP is a $659-billion economic relief program established as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act to help small businesses, self-employed workers, sole proprietors, certain nonprofit organizations, and tribal businesses remain solvent and continue paying their workers during the COVID-19 shutdown. Under the PPP, a qualifying small business (generally with fewer than 500 employees) could obtain a loan of up to $10 million at a very low interest rate (1%) and have the loan forgiven after proving that the money was used for qualified payroll and other expenses.

Earlier this month, the Small Business Administration (SBA)released its PPP Loan Forgiveness Application along with detailed instructions for completing and submitting the application.

The form’s instructions help you understand how to apply for forgiveness of your PPP loan, consistent with the CARES Act. and to simplify the process, the instructions and form include several measures to reduce compliance burdens, including: Continue reading… Continue reading… Continue reading…

It’s Time to Schedule Your Free Annual Financial Tune-Up

Share This Post

Tax and financial planning professionals typically have two busy seasons — the February-April crunch, as clients push to file their taxes by mid-April, and August-October for extensions (mostly corporate filers). This raises the question of where professional like us go and what we do in the summer.

Here at Stees, Walker & Company, LLP, we stay put and continue to work hard for our clients. As your tax and financial planning firm, we take advantage of this lull in the rush to conduct complementary mid-year planning meetings with clients in a more relaxed atmosphere.

Summer is the perfect time for us to discuss a financial tune up, and this year it is especially important since we are all facing unusual financial situations. The next three months give us the best opportunity to listen to your concerns, hear about any opportunities you’re interested in pursuing, and help you prepare approaches to take you from potential crises to recovery and beyond.

As a part of your tax and financial planning team, we listen for what matters to you and what you want your financial future to look like. Once we understand where you’re at financially, and where you want to be in the future, we work closely with you to reduce your tax bill and ultimately increase your net worth.

This year’s complementary mid-year meeting gives us an opportunity to re-evaluate your financial profile and enhance your financial journey by covering a range of topics — all of which are important pieces in your financial profile. During this one-hour meeting, we focus on the following three outcomes: Continue reading… Continue reading… Continue reading…

How to Determine Loan Forgiveness Under the Paycheck Protection Program

Share This Post

The recent $669-billion Paycheck Protection Program (PPP) established by the Coronavirus Aid Relief and Economic Security (CARES) Act has been enacted to a chorus of mixed reviews.

The PPP provides loans of up to $10 million per eligible small business to cover payroll costs and other qualifying expenses (such as rent and utilities) to keep small businesses afloat and employees paid until government agencies allow them to reopen. Perhaps best of all, the total amount of each loan used to cover payroll and qualifying expenses may ultimately be forgiven. In other words, the U.S. government won’t require repayment under certain conditions.

Since banks started taking applications for PPP loans, the program has been plagued with controversy — from big businesses getting the lion’s share of the allocated funds to employers having to contend with furloughed and laid off employees who do not see the value in returning to work because they may be able to earn more by remaining on unemployment.

If your company applied for and was approved for a PPP loan, all of this controversy may be water under the bridge. Now your concern is focused on how much of the money you received in the form of a PPP loan will need to be paid back. This post addresses that concern — both for businesses with employees and for self-employed individuals.

Loan Forgiveness for Businesses with Employees

If you own a business and have employees working for you, the amount of your Paycheck Protection Program loan that will be forgiven is said to be equal to the following payments made, and the costs incurred during the eight-week period beginning on the loan origination date (the first disbursement date):

- Payroll costs:

- Gross salary, wages, commissions, or tips paid to employees (based on an annual wage of up to $100,000 per worker)

- Vacation, parental, family, medical, or sick leave (excluding any family or sick leave covered under the Families First Coronavirus Response Act and reimbursed through payroll tax credits)

- Termination allowances

- Group health care benefits, including insurance premiums

- Retirement benefit payments

- State and local payroll taxes

- Mortgage interest on a mortgage taken out by the borrower for real or personal property incurred prior to Feb. 15, 2020 (not including prepayments)

- Rent on a lease taken out before Feb. 15, 2020

- Utilities for service begun before Feb. 15, 2020

The entire amount of the Paycheck Protection Program loan is supposed to be forgiven if you meet all three of the following conditions: Continue reading… Continue reading… Continue reading…

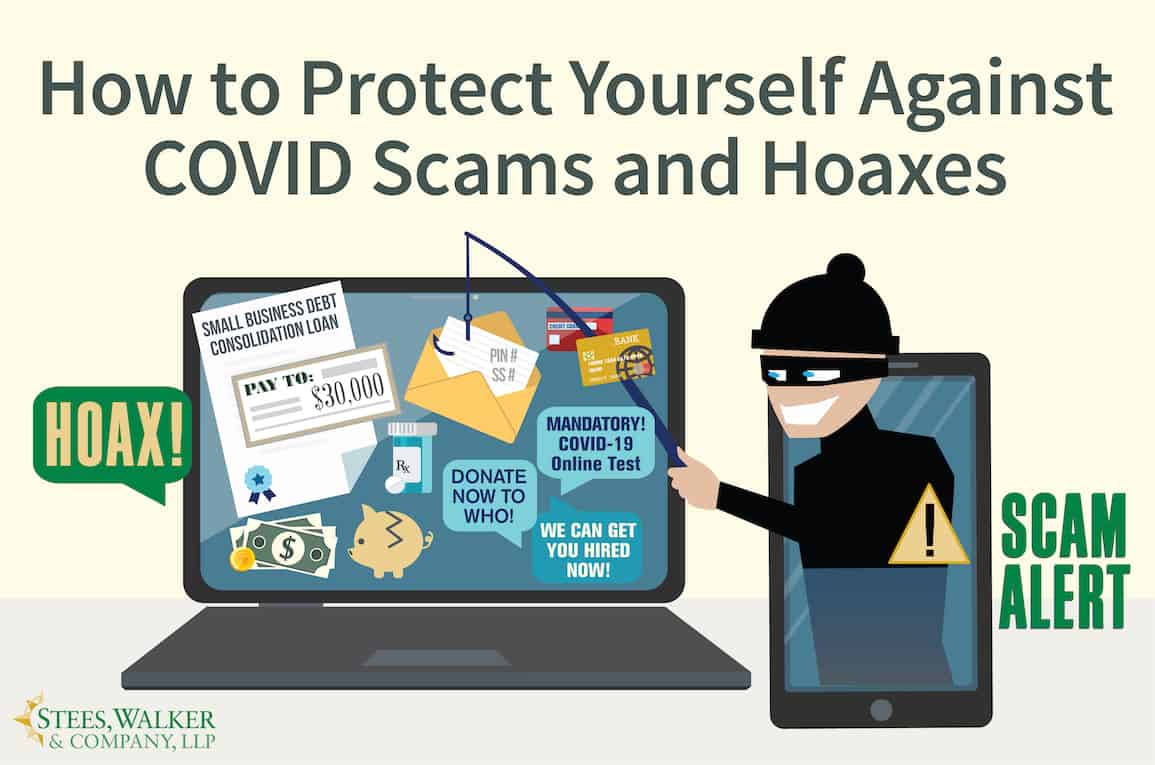

How to Protect Yourself Against COVID Scams and Hoaxes

Share This Post

Run a Google News search for COVID Scam and you’ll find an endless stream of negative articles. These range from a California doctor busted for selling a bogus “miracle cure,” to a staggering number of stories describing pandemic-related malware and phishing email scams in the past two months.

Then there are news alerts from the Federal Trade Commission, Federal Bureau of Investigation, and U.S. Department of Treasury (among others) telling us to avoid being pulled into these scams and rip-offs. It’s not like we don’t have enough on our plates with this pandemic, now we now have to watch out for criminals determined to scam us out of our money — often when we’re at our most vulnerable.

Here at Stees., Walker & Company, LLP we hate to see anyone being suckered by a clever con, so in this post, we offer guidance on how to protect yourself and your money in these difficult times.

Recognizing Common Scams and Hoaxes

One of the best ways to avoid falling victim to a scam or hoax is to recognize how the fraudsters operate. Here are some common scams and hoaxes to beware of:

- Government imposters: “Con” is short for “confidence,” and what elicits more confidence from people than the belief that they’re dealing with a trusted government representative? Con artists often reach out to people via social media, emails, phone calls, and even knocking on their doors, trying to win their confidence. They present themselves as government agents offering to help, and they use greed or fear to trigger impulsive action. For example, a recent text message claiming to come from the “FCC Financial Care Center” offers $30,000 in COVID-19 relief. Another text message impersonating the U.S. Department of Health and Human Services informs recipients that they must take a “mandatory online COVID-19 test” by clicking a certain link. Whenever someone claims to be from the government threatening punitive action or offers to help, tread very carefully.

- Scams related to stimulus payments: Taxpayers should be on the lookout for IRS impersonation calls, texts, and email phishing attempts about the COVID-19 Tax Relief and Economic Impact Payments (the so-called stimulus checks). The con artists involved in these scams are looking to steal your stimulus payment or your identity. Take the following precautions: Continue reading… Continue reading… Continue reading…

Understanding Small-Business Tax Deductions

Share This Post

As part of an effort to mitigate the effects of the spread of the coronavirus known as COVID-19, the Internal Revenue Services has chosen to delay the April 15, 2020 tax filing deadline for most individual taxpayers and businesses to July 15, 2020. Regardless of the deadline, one thing that isn’t expected to change anytime soon is what a business can and cannot claim as a tax deduction. And in today’s post, we offer insight into exactly that — what small businesses can and cannot deduct, regardless of the tax filing deadline.

A deduction (or write-off) is an expense or portion of an expense subtracted from your company’s gross income that reduces the income on which taxes are calculated. Every dollar you claim as a deduction is a dollar less that is subject to federal, state, and local income tax and self-employment tax (Social Security and Medicare).

For example, if your effective federal income tax rate is 25 percent, and you pay 15.3 percent in self-employment tax and 5 percent in state and local income tax, every thousand dollars less you report in taxable income is over 450 dollars you save in taxes: (0.25 + 0.153 + 0.05) x $1,000 = 0.453 x $1,000 = $453.

The Tax Cuts and Jobs Act (TCJA), which became effective in 2018, made it less advantageous for taxpayers to itemize personal deductions. However, if you own a small business — such as a sole-proprietorship, limited liability company (LLC), or partnership — you can deduct a broad range of business expenses to lower the taxable income you earn from that business.

Here are a couple tips for claiming business deductions without getting into legal trouble:

- Seek confirmation from a tax specialist or certified public accountant (CPA) before claiming any business expense as a deduction.

- Keep accurate, detailed records, including invoices and receipts for all business expenses. (Your CPA can help you find accounting packages and apps to simplify your record-keeping.)

In the following sections, we present a long list of common small-business tax deductions. Continue reading… Continue reading… Continue reading…

Estimating Your Paycheck Protection Program Loan Amount

Share This Post

If you’re a small-business owner, sole-proprietor, freelancer, or independent contractor, you may be wondering just how much money you are eligible to borrow under the Paycheck Protection Program (PPP).

For those unfamiliar with the Paycheck Protection Program, it is part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which was signed into law on Friday, March 27, 2020. As of April 3, businesses with fewer than 500 employees, and other entities that qualify as small businesses, are eligible for loans of up to $10 million to keep them afloat and their workers paid for up to eight (8) weeks, without having to pay back the portion of the loan used to cover payroll and other qualified costs — mortgage interest (or rent) and utilities.

The short answer to how much money your business may be eligible to borrow under the Paycheck Protection Program is this:

- You can borrow up to 2.5 times your monthly payroll costs or up to $10 million, whichever is less; however,

- When you apply for a PPP loan, the bank will want a more precise estimate of your payroll costs and other qualified costs.

In this post, we provide some general guidance on estimating your Paycheck Protection Program loan amount based on our interpretation of law. Your bank (or your accountant if you’re not a client of our San Diego Tax Planning Firm) can help you determine the exact amount based on your bank’s interpretation of the law.

Calculate the Maximum Amount You Can Borrow

The Small Business Administration provides the following step-by-step instructions for calculating the maximum amount you can borrow under the Paycheck Protection Program: Continue reading… Continue reading… Continue reading…

Answers to Paycheck Protection Program Questions

Share This Post

Since the Payroll Protection Program (PPP) launched on Friday, April 3, 2020, small-business owners have been hard-pressed to find banks that will accept PPP loan applications. Many banks and small-business owners say they are struggling to understand Small Business Administration (SBA) and U.S. Department of Treasury PPP-related rules and regulations.

In addition to puzzling over these mandates that govern the distribution of funds, banks find themselves scrambling to get personnel and processes in place to properly handle the application and approval process.

Here at Stees, Walker & Company LLP, we are encouraging small-business owners who are waiting for banks to get up to speed on the Payroll Protection Program to make preparations in advance. See last week’s post, “Get Ready for the Paycheck Protection Program NOW!”

For the uninitiated, the Payroll Protection Program was established as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which was signed into law on Friday, March 27, 2020. The PPP has allotted $349 billion to provide small businesses with low-interest loans of up to $10 million per loan to keep them afloat and their workers paid for up to eight (8) weeks.

Sole proprietors, freelancers, and self-employed individuals are also eligible. To qualify, applicants need not put up any collateral or make any personal guarantee of repayment Payments are deferred for up to six months and, most importantly, the portion of the loan proceeds used to cover payroll and qualified operating expenses (which can be up to about 25 percent of the total loan amount) are likely to be forgiven.

Part of the reason for the delay among banks and small-business owners is confusion over the rules and the process. To clarify the rules, on April 7, 2020, the Small Business Administration (SBA) issued clarifications, many of which address how small businesses should determine their payroll costs. Following is a condensed version these clarifications: Continue reading… Continue reading… Continue reading…