Welcome to Part 1 of our 12-part series on how to reduce your tax burden legally. Here in Part 1, we address the first and most important step — tax planning. As the old saying goes, “Failing to plan is planning to fail,” and this is especially true when you are trying to reduce your tax burden legally.

Consider for a moment the first time you drove a car? If you were doing it right, you spent far more time looking where you were going than where you came from. You don’t drive forward staring in the rearview mirror. Unfortunately, that’s how most tax “specialists” are geared. They spend so much time looking back at last year’s finances that they rarely advise their clients to look forward.

They can tell you all about what you earned and spent last year and how much you owe in taxes as a result, but they rarely think to tell you what you should do today to save on taxes next year. Even the few who do tell their clients what to do rarely tell them when or how to do it.

Taking a proactive, forward-looking approach with tax planning can simplify next year’s taxes and save you a considerable amount of money, especially if you’re a small-business owner. Tax planning provides small-business owners with two valuable benefits:

Benefit No. 1: First, tax planning is a key component in your financial protection. As a small to medium size business owner, you have two ways to increase your net profits: financial offense (earning more) and financial defense (spending less). For most small-business owners, taxes are the biggest expense, so a big part of playing financial defense involves reducing the tax burden. And you do that through savvy tax planning.

Benefit No. 2: Second, participating in tax planning almost always ensures results. You can spend a huge amount of time, effort, and money promoting your business with no guarantee of achieving positive results. In contrast, every tax-savings initiative you implement guarantees a return on your investment. But those guaranteed results start with planning. For example, you can’t deduct medical expenses paid out of a medical expense reimbursement plan if you haven’t set up such a plan ahead of time.

To get this series started, indulge us for a moment as we cover how the tax system works here in the United States of America.

Understanding How the Tax System Works

A general knowledge about how the tax system works lays the foundation for understanding specific tax-savings approaches we present later on in this post. Here’s a graphic demonstrating how the tax system works:

- Add your income from all sources to calculate “total income.”

- Subtract “adjustments to income” available to all taxpayers, regardless of whether you itemize, such as certain education expenses and contributions to health savings accounts (HSAs).

- Subtract your standard deduction or total itemized deductions, whichever amount is greater.

- Consult the table of tax brackets to determine your actual tax.

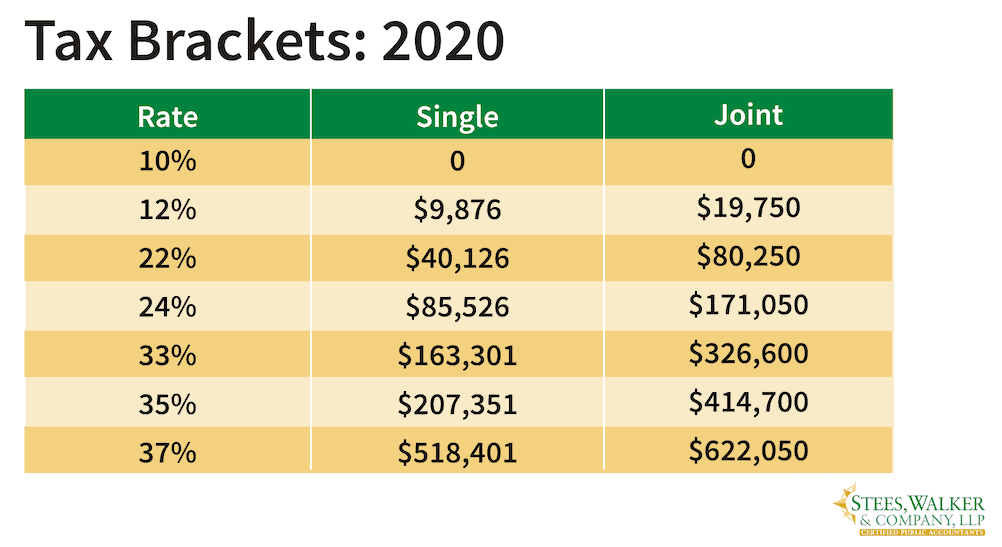

- Note that portions of your income are taxed at different rates; for example, in 2020 if you’re married filing jointly, you pay 10 percent on the first $19,400 of income, 12 percent on the next $59,549, 22 percent on the next $89,449, and so on. The maximum percentage you pay is your marginal tax rate. The average percentage is your effective tax rate.

- Subtract any available tax credits, such as the child and dependent care credit.

- Add any extra taxes such as self-employment tax or net investment income tax.

- Claim your tax refunds or write your checks (if you owe taxes) to the federal, state, and local tax authorities.

Step 1: Calculate your total income

As you may have guessed, the process starts with income, which includes everything that the Internal Revenue Service (IRS) is interested in, including:

- Earned income from wages, salaries, bonuses, and commissions

- Profits and losses from your own business

- Interest and dividends from bank accounts, stocks, bonds, and mutual funds

- Capital gains from sales of property

- Income from pensions, IRAs, and annuities

- Alimony received

- Gambling winnings

As it turns out, even illegal income is taxable. The IRS doesn’t really care all that much how you earn the income. The government just wants its share. In most cases, if you’re operating an illegal business, you’re able to deduct many of the same expenses as if you were running a lawful business. Take bookies for example — they can deduct the cost of a mobile phone used to accept wagers. If however the expenses fall under the notion of being “contrary to public policy” — and most businesses involving illegal drugs, like a marijuana business, even if it’s legal in the state in which you’re operating the business, it is federally illegal — you’re prohibited from deducting expenses related to that business.

Step 2: Subtract your adjustments to income

Next, you subtract “adjustments to income,” which are considered special deductions, listed on the first page of Form 1040 (officially, the “U.S. Individual Income Tax Return”) that you can take whether you itemize deductions or not. These include:

- One-half of self-employment tax

- Self-employed health insurance

- Contributions to an IRA account

- Student loan interest up to $2,500

- Moving expenses (for active duty military personnel only starting in 2018)

- Alimony payments (for agreements entered into before January 1, 2019)

Total income minus adjustments to income equals “adjusted gross income” or AGI. These are also called “above the line” deductions, because you take them “above” the line that separates total income from AGI.

Step 3: Subtract your standard or itemized deductions

After you’ve calculated your adjusted gross income, it’s time to take your standard deduction or itemized deductions, whichever is more. For 2020, the standard deduction amounts are $12,400 for singles, $18,650 for heads of households, $24,800 for married couples filing jointly, and $12,200 for married individuals filing separately. (Note: Approximately 90 percent of taxpayers claim the standard deduction.)

If your total itemized deductions exceed the standard deduction for which you qualify, itemizing will save you money. Unfortunately, you need to crunch the numbers to find out, and you may do all that extra work only to discover that itemizing isn’t the best option.

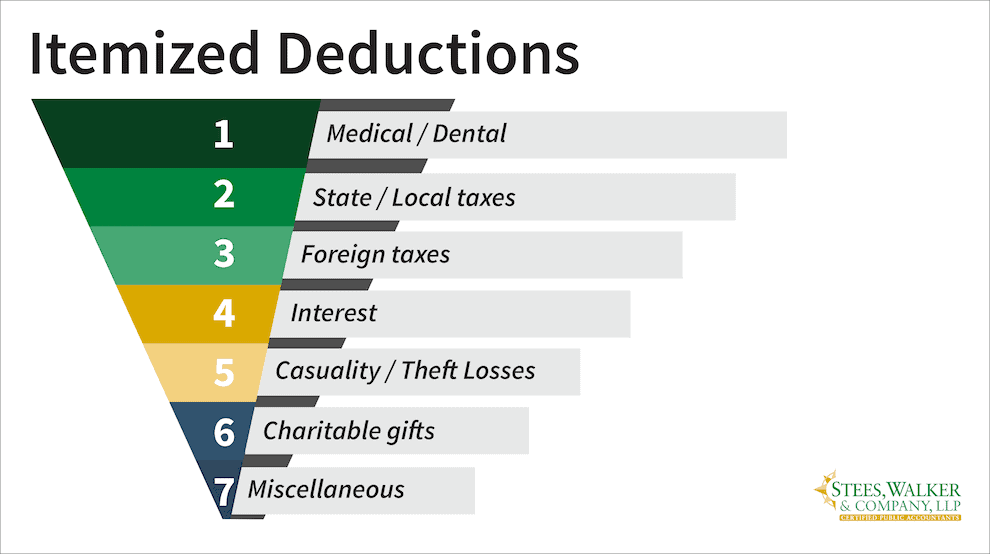

To find out whether itemizing will reduce your tax bill, total the following:

- Medical expenses, to the extent they top 7.5 percent of your AGI

- State and local income, sales, and property taxes paid (up to a total of $10,000 per year)

- Foreign taxes paid

- Mortgage interest on up to $1 million for loans closed before December 15, 2017, or $750,000 for loans closed after that date

- Casualty and theft losses incurred as a result of a federally declared disaster, to the extent they exceed 10 percent of your adjusted gross income

- Charitable contributions

As you would expect, tax deductions reduce your taxable income. If you’re in the 12 percent bracket, an extra dollar of deductions cuts your tax by 12 cents on the dollar. If you’re in the 35 percent bracket, that same extra dollar of deductions cuts your tax by 35 cents on the dollar.

Step 4: Consult the table of tax brackets

After subtracting deductions from your adjusted gross income (AGI), you’re left with your “taxable income,” which determines the rate(s) at which your income is taxed.

Suppose you’re single, and your taxable income is $100,000. Here’s how your taxes on that amount would be calculated:

- $9,875 x 0.10 = $987.50

- $30,249 x 0.12 = $3,629.88

- $45,399 x 0.22 = $9,987.78

- $14,474 x 0.24 = $3,473.76

- TOTAL TAX = $18,078.92

So, your effective tax rate is $18,078.92/$100,000 = 18.08 percent

Step 5: Subtract your tax credits

Finally, you subtract available tax credits. These are dollar-for-dollar tax reductions that you’re allowed to take advantage of regardless of your tax bracket. For example, if you have $2,500 total in tax credits, your tax bill is reduced by that amount:

$18,078.92 – $2,500 = $15,578.92

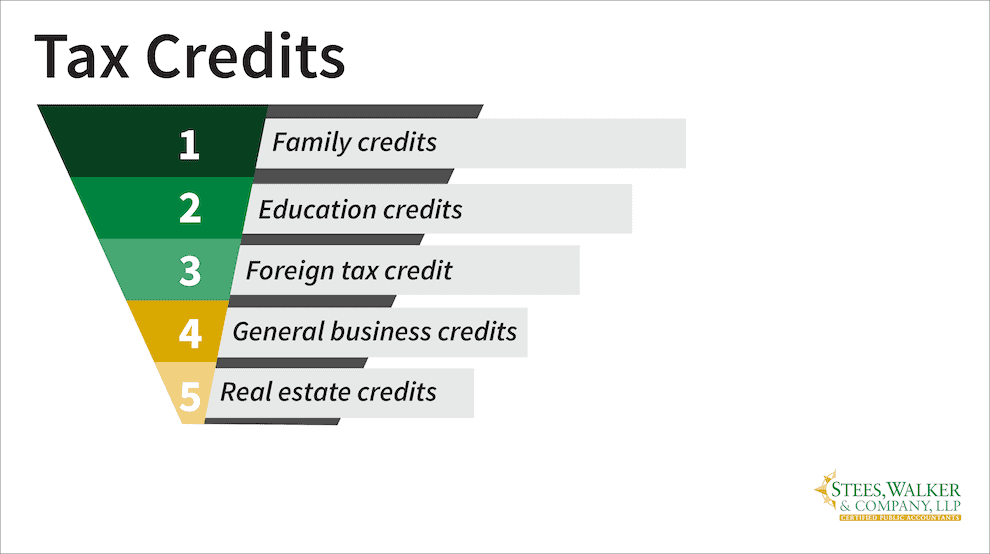

Despite what you may have heard, there’s no secret to using tax credits, other than knowing what’s available to you. While dozens of tax credits are available, they tend to fall into five main categories:

- Family credits, such as the Child Tax Credit and Dependent Care Credit

- Education credits, such as the American Opportunity Credit and Lifetime Learning Credit

- Foreign tax credits for taxes paid to foreign countries

- General business credits for all sorts of business expenses, such as research & development, hiring employees from disadvantaged groups, and pension plan startup expenses

- Real estate credits, such as the low-income housing credit and renovation credit

These credits can be quite substantial. For example, the child tax credit is $2,000 per child (up to age 17), with the threshold for phasing it out at $200,000 for single filers and $400,000 for joint filers.

Step 6: Add any extra taxes

Almost done! We’ve taken care of income taxes, but you may be on the hook for other taxes, as well, such as the following:

- Self-employment tax, which is what self-employed people pay in place of Social Security and Medicare taxes.

- A 3.8 percent net investment income tax on investment income, which the Patient Protection and Affordable Healthcare Act introduced in 2013. This tax hits single taxpayers earning more than $200,000 and joint filers earning more than $250,000. For purposes of this rule, “investment income” includes interest, dividends, capital gains, rental income, royalties, and annuity distributions.

- The alternative minimum tax (AMT) for people deemed by the government to be paying too little income tax after accounting for all their deductions and credits.

- The so-called nanny tax to cover Social Security and Medicare taxes for any household employees being paid over a certain minimum amount.

The bottom line here is that “tax brackets” aren’t as simple as they might appear. Your actual tax rate may be higher than the tax rate based solely on your adjusted gross income.

So that’s how the system works. (Pretty simple, right?)

Leveraging the Power of Tax Planning to Game the System

Knowing how the system works opens opportunities for reducing your tax burden, but to take advantage of these opportunities, you must plan ahead and perform certain tasks during the tax year. And that’s where a tax and financial planning firm like Stees, Walker & Company, LLP can help.

Waiting until it’s time to prepare your taxes is often too late. Here are a few tax-reduction approaches that require planning ahead and taking action throughout the tax year:

- Incorporate your business or change its business structure. For example, with an S Corporation, you can get money out of the business in two forms — as wage income (subject to Social Security taxes), and as distributions (not subject to Social Security taxes). Properly planning for type of income will reduce the amount you pay in self-employment tax.

- Pay yourself in part with tax-free fringe benefits, including medical coverage, health savings account, and a retirement plan.

- Set up a medical expense reimbursement plan through an eligible business, so you can pay all medical expenses for you and your family with untaxed dollars.

- Hire relatives to work for you, thereby reducing your income by the amount you pay them, all while shifting your tax burden to a lower tax bracket.

- Set up regular contributions to a tax-deferred retirement account. You can contribute to these accounts up to the tax year’s filing deadline, but many people don’t have anything set aside at the end of the year to make a substantial contribution.

- Set up a health savings account (HSA) and fund it.

Stay tuned for future posts in our 12-part series on how to reduce your tax burden legally, in which we cover these, and other tax-savings approaches in greater depth. But first, we’re going to explain how to “audit proof” your tax return. That is the topic for next week’s post.

– – – – – – – – –

Disclaimer: The information in this blog post about tax planning, is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment