The Affordable Care Act (ACA), dubbed “Obamacare,” made health care much less affordable for many small-business owners. It led to higher health insurance premiums, while doing little to nothing to rein in the spiraling costs of doctor visits, diagnostic tests, pharmaceuticals, and hospital care.

As a result, many small-business owners have dropped their healthcare coverage, which is not something we recommend. That’s because a single unforeseen individual or family illness could stick you with a bill that could drive you into bankruptcy. What we do recommend is that you make healthcare more affordable for yourself and your family by taking full advantage of every tax break available for healthcare expenses.

You are probably already aware that if you pay for your own health insurance, you’re allowed to deduct it as an adjustment to income. You’re probably also aware that if you itemize your deductions, you’re allowed to deduct unreimbursed dental and medical that exceed 7.5 percent of your adjusted gross income. However, most of us don’t spend that much on healthcare, and since the standard deduction nearly doubled with the passing of the Tax Cut and Jobs Act of 2017, many of us don’t itemize. As a result, we end up losing a lot of money in otherwise legitimate deductions.

Here’s an idea. What if there was a way to write off medical bills as business expenses? Actually, there are three ways:

- Medical Expense Reimbursement Plan (MERP)

- Health Savings Account (HSA)

- Flexible Spending Account (FSA)

Pro Tip: Take a big-picture approach to healthcare costs. While a high-deductible healthcare plan costs less and makes you eligible to contribute to a health savings account (HSA) and pay out-of-pocket costs out of that account tax-free, a low-deductible plan that covers more expenses may be more cost-effective for your family depending on your situation. Here at Stees, Walker & Company, LLP, we can help you evaluate different plans and choose a plan that’s best for your overall finances.

In any event, in this post we cover each of the three ways to legally write off medical bills as business expenses, starting with the use of an MERP (medical expense reimbursement plan).

Medical Expense Reimbursement Plan (MERP)

The first thing to know about a MERP (also known as a 105 plan) is that it’s an employee benefit plan. That means it requires an employee:

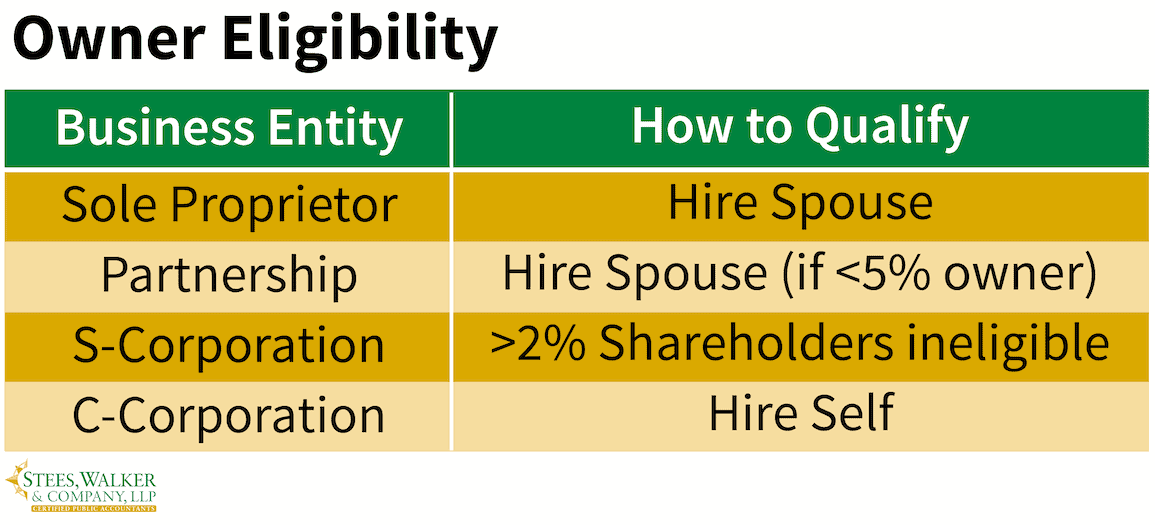

- If your business is taxed as a sole proprietorship, you’re considered self-employed. You can’t establish the plan for yourself. However, if you’re married, you can hire your spouse.

- If your business is taxed as a partnership, you’re also considered self-employed. Again, you can’t establish the plan for yourself. However, you can still hire your spouse so long as he or she owns less than 5 percent of the business.

- If your business is taxed as an S corporation, both you and your spouse are considered self-employed. This means you’ll need another source of income, not taxed as an S corporation, to establish the plan. (Alternatively, you can establish a health savings account, covered later in this post, to give yourself most of the same benefit as the 105 plan.)

- If your business is taxed as a C corporation, you qualify as your own employee, so you can simply hire yourself.

If you’re married, and you choose to hire your spouse, you don’t even have to pay him or her a salary. You can compensate them in the form of benefits only, which avoids the hassle of filing payroll returns. The main requirement here is that the benefits you pay have to be “reasonable compensation” for the service they perform. If your spouse works an hour a month filing invoices for you, you’ll probably have a hard time convincing an auditor that that’s “reasonable” for $4,000 worth of LASIK surgery!

Eligible Expenses with a MERP

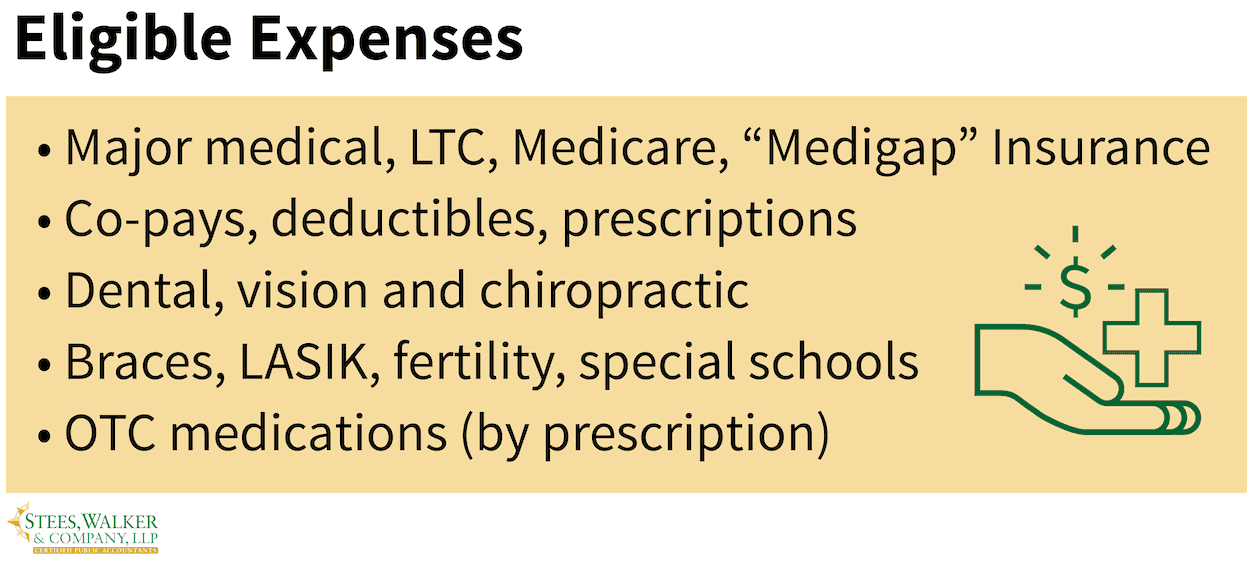

Once the MERP is in place, you can reimburse your employee for any medical expense they incur for themselves, their spouse, and their dependents, including the following:

- Any kind of health insurance, including major medical, long-term care (up to specific Internal Revenue Service limits), Medicare premiums, and even Medigap coverage.

- All copays, deductibles, “co-insurance,” and other amounts insurance doesn’t pay.

- All prescription medications.

- Expenses for dental care, vision care, and chiropractic care that traditional insurance might not cover.

- Some big-ticket expenses such as orthodontist care (braces for children), fertility treatments, and special schools for learning-disabled children. Let’s say your physician diagnoses your 8-year-old son with ADHD, and prescribes tai kwon do lessons. Guess what – those lessons are now tax-deductible!

- Over-the-counter medications and supplies, so long as they’re prescribed by a physician.

One big advantage of the medical expense reimbursement plan is that it works with any insurance policy. You don’t have to purchase special coverage. You can use a MERP with insurance you buy on an exchange or on your own. If your spouse receives coverage from their employer, you can even set up a MERP in your business to cover any out-of-pocket expenses your spouse’s insurance doesn’t cover.

Say for instance that you’re a sole proprietor with three children and you’ve hired your spouse to work for your business. The MERP lets you reimburse your employee/husband for all dental and medical expenses he incurs for himself, his spouse (which brings you into the plan), and his dependents — your kids.

This includes all the eligible expenses listed below.

The best part is, this is money you’d spend anyway, regardless of whether you’d claim it as a deduction. You’ll spend your money on contact lenses or your kids’ braces whether it’s deductible or not. The MERP simply allows you to move it from someplace on your return where you certainly can’t deduct all of it (and probably can’t deduct any of it), to a place where you can.

Setting Up and Using a MERP

Setting up a medical expense reimbursement plan (MERP) starts with a written document — a plan, if you will, which we here at Stees, Walker & Company, LLP can draft for you.

If you’ve hired your spouse, you’ll need to be able to verify that they qualify as a bona fide “employee.” That means you need to direct the work they perform for the business, the same as you would direct the work that any other employee performs.

Here’s one important requirement that the IRS will pay attention to in the unlikely event you’re audited — youmust run the payments through the business. You can’t just pay medical bills out of the family personal account, total them up at the end of the year, and throw them on the business return.

This means you have two choices:

- Pay healthcare providers directly out of the business account. If your business account has a debit card or you have a business credit card, you can use it to charge medical expenses directly to the business.

- Reimburse your employees (from the business account) for expenses they pay out of their personal funds. For example, suppose your husband picks up a prescription. He can use his own money, and you can reimburse him from the business account.

If you’ve simply hired your spouse in order to write off your own family’s medical expenses, you generally don’t need a third-party administrator (TPA), but you will need a TPA if you’re reimbursing non-familyemployees (to avoid violating medical privacy rules).

No pre-funding is required. You don’t have to open a special bank or investment account, as you do with a health savings account or flexible spending account. You don’t have to decide up front how much to contribute to the plan, as you must do with flexible spending accounts, and there’s no “use it or lose it” rule. The MERP is really just an accounting device that lets you recharacterize your family medical bills as a business expense.

The MERP doesn’t just help you save income tax. It also helps you save self-employment tax. Remember, when you work for yourself, you pay a self-employment tax in place of the Social Security and Medicare taxes that you and your employer would share on your salary. That self-employment tax is based on your “net self-employment earnings.” Using a MERP, all medical expenses reduce your self-employment income, so you’re not paying self-employment tax on that money.

Determining Employee Eligibility

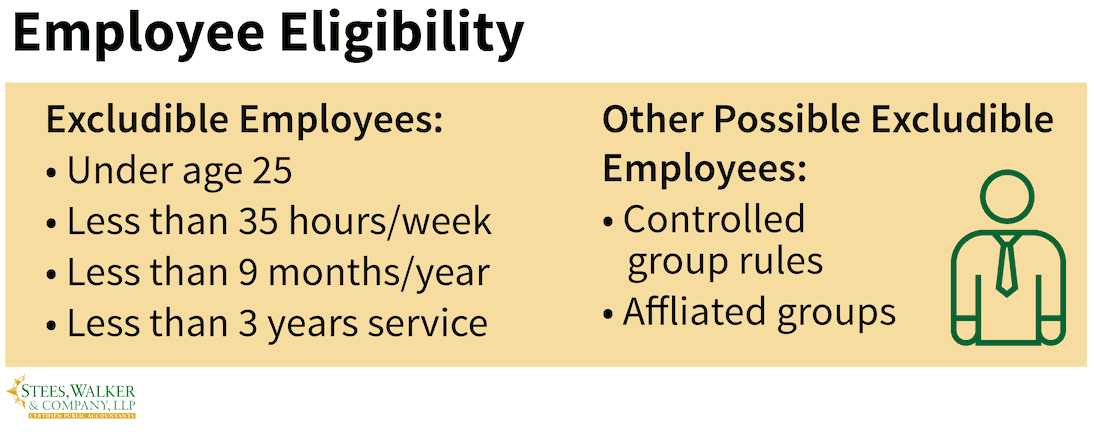

Here’s the not so good news. If you have non-family employees, you must include them. To be sure, you can exclude employees under age 25 who work less than 35 hours per week and less than nine months per year, or who have worked for you less than three years. You can also exclude employees covered by a collective bargaining agreement that includes health benefits. Regardless, having non-family employees may make it prohibitively expensive to reimburse everyone as generously as you’d cover your own family.

One final formality: The Affordable Care Act imposed a pesky excise tax requirement on MERPs called the “Patient Centered Outcomes Research Trust Fund Fee,” or PCORI fee. For plan in the years ending after September 30, 2019 and before October 1, 2020, that amount is $2.54 per person, which gets reported on IRS Form 720, and is due by July 31, 2021.

Next up among the three ways to legally write off medical bills as business expenses is the health savings account (HSA).

Health Savings Accounts (HSAs)

If a medical expense reimbursement plan isn’t appropriate — either because you don’t have a spouse to hire or you have non-family employees you would have to cover — consider establishing a health savings account (HSA). These arrangements combine a high-deductible health plan with a tax-free savings account to cover unreimbursed costs.

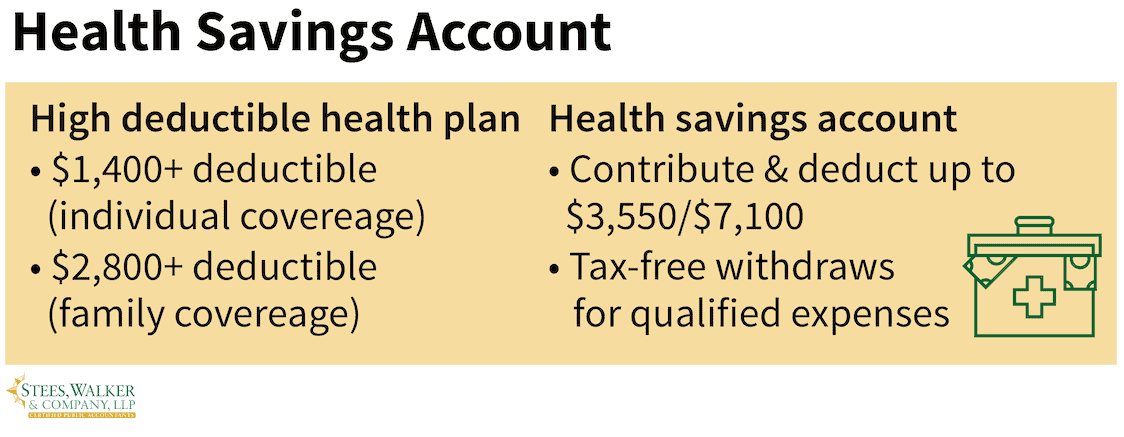

To qualify, you’ll need to be covered by a high-deductible health plan (HDHP). For 2020, this means the deductible is at least $1,400 for single coverage or $2,800 for family coverage. Neither you nor your spouse can be covered by a “non-high deductible health plan” or by Medicare. The plan can’t cover any expense, other than certain preventive care benefits, until you satisfy the annual deductible. You’re not eligible if you’re covered by a separate plan or rider offering prescription drug benefits before the minimum annual deductible is satisfied.

Once you’ve established your eligibility, you can open a deductible health savings account at your bank to cover out-of-pocket expenses (those not covered by your insurance). For 2020, you can contribute up to $3,550 if you have individual coverage or $7,100 if you have family coverage. (If you’re 55 or older, you can contribute an extra $1,000 per year.)

HSAs are easy to open. Most banks, brokerage firms, and insurance companies offer them, and many will issueyou a debit card, so you can charge medical expenses directly to the account.

Generally, you’re prohibited from using funds in your HSA to pay health insurance premiums. These funds are for paying out-of-pocket (OOP) costs. You can use your HSA to pay health insurance premiums only if you are collecting federal or state unemployment benefits or you have Consolidated Omnibus Budget Reconciliation Act (COBRA) continuation coverage through a former employer.

Withdrawals are tax-free so long as you use them for “qualified medical costs.” Withdrawals not used for qualified medical costs are subject to regular income tax plus a 20 percent penalty. When you reach the age of 65, withdrawals are no longer subject to the 20 percent penalty, but they’re still subject to regular income tax.

After your passing, your HSA account goes to your specified beneficiary. And if your beneficiary is your own spouse, they are allowed to treat it as an HSA of their own. And if they choose not to, your beneficiary will pay ordinary tax on the account proceeds (but not the 20 percent penalty).

The health savings account (HSA) isn’t quite as powerful or flexible as the medical expense reimbursement plan (MERP). You have specific dollar limits on what you can contribute to the account, which might not cover allyour out-of-pocket costs. And there’s no self-employment tax advantage as there is with a MERP. However, an HSA can still help cut your overall healthcare costs by allowing you to deduct those costs.

Finally, your third option for legally writing off medical bills as business expenses is the flexible spending account.

Flexible Spending Accounts (FSA)

Flexible spending accounts (FSAs) are available to those that work for an employer that offers this benefit, which is another way of saying these plans are not available to those classified as being self-employed.

Flexible spending accounts let you set aside pre-tax dollars (up to $2,750) for a variety of nontaxable benefits, including medical expense reimbursement, and disability and health insurance. FSA plan contributions avoid federal income and self-employment tax. Your employer deducts plan contributions from your paycheck and deposits them into your account until you claim your reimbursements. Your employer can also match your contributions up to $2,750 but is not required to do so.

Once the money is in the account, you can use it for most medical expenses except nonprescription drugs and supplies, long-term care coverage, and associated expenses.

When you enroll, you must choose how much to contribute each pay period. You generally can’t change your contribution amount in the middle of the plan year unless there’s a change in your family status. Eligible changes include marriage or divorce; birth, adoption, or death of a child; spousal employment; change in a dependent’s student status; and the like.

You can claim your full year’s reimbursement as soon as you incur qualifying expenses, whether you’ve fully funded your account for that amount or not.

Historically, FSA rules have required you to use your account balance by the end of the year or forfeit it. However, employers can provide a grace period of up to two and a half months after the end of the year to use the money, or they can allow employees to carry over up to $500 to the following year.

Now that you have Uncle Sam covering a larger portion of your healthcare costs, consider another tax savings tactic to get him to cover a portion of your home office expenses. Tune in next week for Part 8 of our Small Business Guide to Reducing Your Tax Burden Legally — “Maximizing Your Home Office Deduction.”

– – – – – – – – –

Disclaimer: The information in this blog post about writing off medical bills as business expenses is provided for general informational purposes only and may not reflect current financial thinking or practices. No information contained in this post should be construed as financial advice from the staff at Stees, Walker & Company, LLP, nor is this the information contained in this post intended to be a substitute for financial counsel on any subject matter or intended to take the place of hiring a Certified Public Accountant in your jurisdiction. No reader of this post should act or refrain from acting on the basis of any information included in, or accessible through, this post without seeking the appropriate financial planning advice on the particular facts and circumstances at issue from a licensed financial professional in the recipient’s state, country or other appropriate licensing jurisdiction.

Leave A Comment