Welcome to Our Blog

We’re a San Diego, Calif.-based boutique tax consulting firm focused on personalized tax and financial guidance to individuals and businesses. Here on our blog, you’ll find you’ll find news, insights, and observations from trusted sources in the world of tax planning and and financial guidance.

Designating Yourself a ‘Real Estate Professional’ and Claiming Real Estate Losses Against Ordinary Income

Share This Post

Welcome to the world of real estate, where savvy individuals who have earned the right to call themselves real estate investors have more options for taking advantage of tax-saving opportunities.

For those involved in the real estate industry, “materially participating” in the management of your properties or investments and being classified as a “real estate professional” can translate to substantial tax savings, leaving you with more cash to build your real estate investment portfolio.

In this post, we explore the distinct tax advantages that come with material participation and being recognized as a real estate professional, delving into how these designations can increase deductions, minimize tax liability, and ultimately enhance your financial portfolio of real estate investments.

Whether you’re a seasoned investor or a newcomer eager to optimize your tax planning, understanding and harnessing the potential of these classifications can accelerate your progress toward meeting your real estate investment goals and your overall financial goals.

Claiming Real Estate Losses Against Ordinary Income

As real estate investors know, rental real estate is ordinarily a “passive” activity. Generally, when you’re preparing your tax return, you can deduct passive losses only from passive income — income from sources such as stocks, mutual funds, royalties, and rental properties. You’re generally not allowed to deduct passive losses against ordinary income — income from sources such as salary and interest.

If all your income is passive, or if your passive gains exceed your passive losses, this restriction doesn’t impact your tax obligation. However, if your passive losses exceed your passive gains, and you have ordinary income, being able to claim passive losses against ordinary income can reduce your tax obligation.

There are two important exceptions that allow you to claim passive losses against ordinary income: Continue reading… Continue reading… Continue reading…

What You Need to Know About the Research and Development Tax Credit

Share This Post

When we initially meet with small business clients, they sometimes lament that the federal government isn’t as supportive of their contributions to society as they’d like. They envision a world where innovation not only fuels their business growth but also earns them a significant tax break.

As it turns out, in some respects, this is already a reality. The Credit For Increasing Research Activities (aka, the Research and Development (R&D) Tax Credit) — which first appeared as part of the Economic Tax Recovery Act of 1981 — is an often-overlooked tax incentive that serves as a powerful tool that may put money back into your business’ pocket for the inventive work you’re already doing. In this blog post, we share what you need to know to take advantage of this important tax credit.

If any part of your business involves designing, developing, or improving products, processes, formulas, or software, be sure you’re claiming a federal Research and Development (R&D) Tax Credit and any R&D tax credits your state may be offering to offset the costs of these activities. The federal benefit provides a dollar-for-dollar credit against your business tax for the costs of performing R&D activities.

Qualified expenses include:

- W2 wages paid to employees involved in the R&D activity

- Supplies (including tangible property, extraordinary utility costs, and server leasing costs) used for the R&D activity

- Contract R&D-related costs that would qualify if they were conducted by regular employees

Qualifying for the R&D Tax Credit: The Four Criteria

To qualify for the Research and Development (R&D) Tax Credit, your company’s R&D activities must be conducted within the United States and must meet all of the following four criteria: Continue reading… Continue reading… Continue reading…

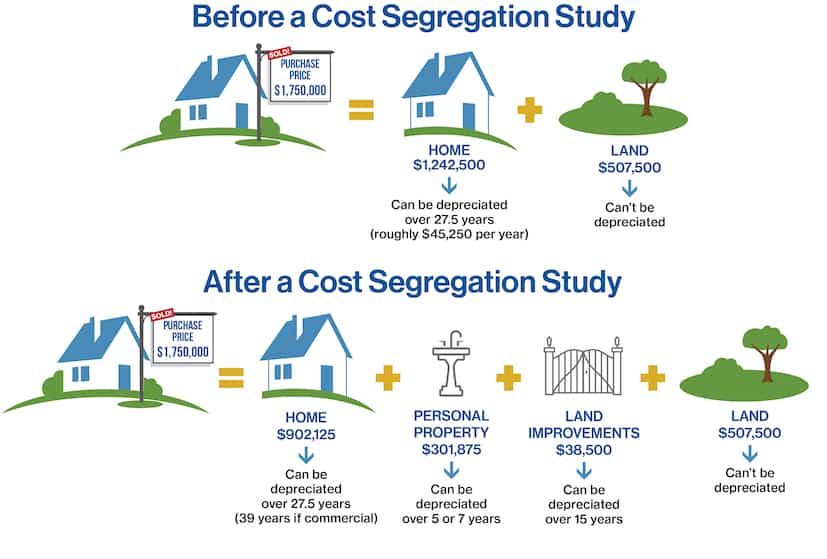

The Pros and Cons of a Cost Segregation Study

Share This Post

If you own real estate, or you’re interested in investing in real estate as a strategy for building or increasing your net worth, then you need to know about cost segregation.

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

Cost segregation is a technique recommended by a tax planning firm that specialize in helping its clients reduce their taxes and increase their net worth. Cost segregation allows property owners and real estate investors to reallocate the costs of a property from long-term assets (which have a useful life of 27.5 years or more) to shorter-lived assets (which have a useful life of less than 27.5 years).

This reallocation can provide significant tax benefits because shorter-lived assets are eligible for accelerated depreciation.

Depreciation 101: Depreciation is an accounting technique that distributes the cost of tangible assets such as real estate over their useful lifespan. It reflects the portion of an asset’s value that’s been utilized, allowing you to gradually pay for and generate revenue from an asset over a specified period of time.

When a property is built or purchased, the costs of the property (such as construction costs or the purchase price and cost of improvements) are typically allocated to the building and land as long-term assets. However, many of the items within a property (such as carpeting, lighting fixtures, and appliances) have a shorter useful life and can be classified as personal property. By identifying these shorter-lived assets and reclassifying them as personal property, the costs associated with them can be depreciated over a shorter period, resulting in a larger tax deduction in the early years of ownership.

Starting With a Cost Segregation Study

To add cost segregation to your tax planning approach, start by ordering a cost segregation study from a reputable firm. Here at SWC, we work with several of these firms and can recommend the right one for your particular circumstances and objectives.

When you engage a firm in a cost segregation study, a cost segregation specialist identifies and reclassifies the costs of your property, typically by examining the property and its invoices, blueprints, and other documentation. The study then allocates property costs to real property or personal property. Findings from the study can then be used by your tax planning firm — in this case, SWC — to calculate a one-time catch- adjustment. That’s because the IRS allows the Continue reading… Continue reading… Continue reading…

New Tax Credits Can Offset the Costs of Energy-Efficient Home Improvements

Share This Post

With energy costs soaring, some homeowners are looking for ways to make their homes more energy efficient. However, energy-efficient home improvements can be quite costly.

To make these improvements more affordable, the federal government offers tax credits to offset the costs, while some state and local governments offer additional tax credits. Thanks to the Inflation Reduction Act of 2022, two substantial federal income tax credits for energy-efficient home improvements have been extended and expanded:

- The residential clean energy credit

- The energy efficient home improvement credit

In this post, we cover these credits and the steps you need to take to claim them.

The Residential Clean Energy Credit

The federal income tax credit for eligible energy saving home improvements, formerly called the residential energy efficient property credit, is now called the residential clean energy credit. Before explaining how the credit has changed, let’s look at how it works under the “old rules” for eligible home improvements made in 2020–2022.

The Old Rules — for 2020–2022

The residential energy property credit varies, depending on when you had the work done:

- 26 percent of qualified expenditures for energy-saving home improvements in 2020–2021

- 30 percent of qualified expenditures for energy-saving home improvements in 2022 (thanks to the Inflation Reduction Act)

Note that there are no income limits. Even billionaires can take advantage of these tax credits. And given the high cost of many energy-saving home improvements, this tax credit can be substantial. For example, the credit for installation of a new $35,000 geothermal system in 2022 is $10,500!

Qualified expenditures include costs for site preparation, assembly, installation, piping, and wiring for the following: Continue reading… Continue reading… Continue reading…

Breaking Up Is Hard to Do: Ending Your California Residency

Share This Post

For more than a dozen years now, more people have been moving from California to other states than have been moving to California from other states. This trend has been attributed to several factors, including cost of living to politics and highway traffic.

Compounding the problem is the fact that many companies — small business and large corporate enterprises alike — are abandoning California due to the high cost of doing business in the state, including Tesla Motors, Kaiser Aluminum, Wiley X Sunglasses, and Gordon Ramsay North American Restaurants.

Some people — especially high-net-worth individuals — want the best of both worlds. They love living in the Golden State for its weather, scenery, culture, culinary options, outdoor activities, and more. However, they would prefer lower taxes and a more business-friendly environment offered by other states such as Texas, Nevada, Florida, and Tennessee.

In an attempt to build this Shangri-La for themselves, they purchase a condo in Las Vegas, San Antonio, Nashville, or Fort Walton Beach and live there instead of in the house they own in California, in the mistaken belief that’s all it takes to reduce or even eliminate their obligation to pay California taxes.

Unfortunately, it’s not that easy. Ending your California residency is much more complicated than just moving out of state. And if you fail to meet all the requirements of becoming a non-resident, you’re likely to be pursued by the State of California’s Franchise Tax Board (FTB) for unpaid taxes and penalties.

In this post, we explain the rules that govern residency in California and what you need to do to officially end your State of California residency.

Defining “Residency”

According to the State of California, a resident is any individual who meets either of the following criteria: Continue reading… Continue reading… Continue reading…

Thanks, Inflation! Cashing in on Inflation-Driven Tax Breaks

Share This Post

Recently, inflation has commandeered the news cycle. Everyone’s worried about it. And why wouldn’t they be? With inflation, everything costs more, and increased income usually lags far behind.

But inflation isn’t all bad. If you own a home, for example, inflation will eventually increase its value (in most cases). And if you have a mortgage on that home, you’ll be paying it off with dollars that aren’t worth nearly as much as the dollars you borrowed.

In addition, inflation can save you money on taxes. “How so?” you ask. In this post, we reveal several ways where inflation has recently resulted in lowering taxes (for some people).

Inflation-Driven Tax-Relief Baked into the Tax Code

Most people assume that inflation will increase their tax burden. Since income taxes are based on income, and if your income increases, you’ll pay more in taxes, right? You might even suffer a double whammy, paying more tax on higher income and getting boosted into a higher tax bracket.

While that’s true to some extent, the tax code has some protections built in that prevent rising prices from automatically triggering higher taxes. In fact, the Internal Revenue Service (IRS) recently announced that thanks to inflation, taxpayers can expect the following relief in 2023 (the following generally applies to tax returns filed in 2024):

- Income thresholds will be increasing 7 percent for all tax brackets. For example, instead of paying the lowest tax rate of 10 percent tax on the first $10,275 you earn, you’ll pay 10 percent on the first $11,000 you earn. If you’re married filing jointly, instead of paying 10 percent on the first $20,250 you earn, you’ll pay 10 percent on the first $22,000 you earn. In other words — assuming you earn the same amount in 2023 as you did in 2022 — you’ll actually be paying less federal income tax.

- The standard deduction is increasing 7 percent from $12,950 for individual filers in 2022 to $13,850 in 2023, and from $25,900 for married couples filing jointly in 2022 to $27,700 in 2023. This represents the largest adjustment to deductions since 1985, when the IRS began annual automatic inflationary adjustments. You’ll start to see the new figures reflected in your income tax withholding statements on paychecks beginning in January 2023, resulting in an increase in take-home pay.

- The maximum Earned Income Tax Credit, one of the federal government’s main anti-poverty measures, will increase from $6,935 in 2022 to $7,430 in 2023.

- The annual gift tax exclusion (the maximum amount one person can give to another without incurring a tax penalty) will increase from $16,000 in 2022 to $17,000 in 2023.

- The estate tax threshold (often used by wealthy Americans to shield inherited assets from levies) will increase from $12.1 million in 2022 to $12.9 million in 2023.

- The amount of income adoptive parents can shield from taxes will increase from $14,890 per child in 2022 to $15,950 per child in 2023.

You May Now Qualify for the Premium Tax Credit

Thanks to the soaring costs of “affordable” health insurance premiums, you may now qualify for the Premium Tax Credit where in recent years, you fell short of the cutoff.

Starting next year, if your Continue reading… Continue reading… Continue reading…

Year-End Tax-Savings Tips for Small-Business Owners and Entrepreneurs

Share This Post

Here at SWC, we’re currently meeting with clients to project what they’re likely to owe in 2022 and discuss ways that they can reduce their tax liability for this year and beyond. In preparation for these meetings, it’s always a good idea for clients to start thinking about steps they can take to lower their upcoming tax bill.

Last week, we presented 6 Personal Tax Savings Steps for Individuals to Take Now — Before End of Year 2022. This week, we turn our attention to tax-savings tips for small-business owners and entrepreneurs.

With only about two months remaining in 2022, time is quickly running out to take advantage of a few attractive tax deductions/credits available only to business owners and entrepreneurs. If you’re planning to delay taking on certain expenses until 2023, you may want to reconsider your approach after reading this post. Some deductions/credits may not be available in 2023, or they may be significantly reduced.

Take advantage now of larger deductions for business meals.

There are four steps that — if you take now — could result in considerable tax savings.

Step 1: Maximize your retirement plan contributions.

If your business already has a retirement plan, consider maximizing tax-deductible contributions before the end of the year. If your business doesn’t have a retirement plan, now’s a good time to consider starting one. With a retirement plan in place, you can make tax-deductible contributions to the plan that grow tax-free until the funds are withdrawn. A retirement plan is a great way for you and your employees to build wealth while reducing your tax burden.

You can set up various types of retirement plans, including the following: Continue reading… Continue reading… Continue reading…

6 Personal Tax Savings Steps to Take Now — Before End of Year 2022

Share This Post

For better or worse, 2022 is coming to an end. Halloween has come and gone, and we’re now seeing Christmas decorations on display at Walmart and other major retailers. Always a sign that tax season is fast approaching.

As the big box stores ramp up for the fall and winter holidays, our focus is on projecting what our clients will be required to pay in federal, state, and local income taxes — and, more important, helping them minimize their tax liability.

The good news is that making year-end tax projections for 2022 will probably be less complicated than in recent years. The Inflation Reduction Act of 2022, which was signed into law in August this year, was a slender version of the tax changes that were initially proposed, and with midterm elections just around the corner, members of Congress aren’t likely to stir the pot by introducing any new tax legislation.

While we think it’s unlikely that individual income tax rates are going to increase soon, if any tax legislation does occur in 2023, we believe the changes are likely to be forward-looking. That being said, when it comes to Congress, we can’t predict anything with certainty.

What we can do is provide individual filers with tax-savings guidance you can count on and start to put into action right now. As you prepare for your 2022 Year-End Tax Planning Meeting (between now and Dec. 16 for SWC clients), take the following steps to start thinking about ways to reduce your tax liability. In next week’s post, we’ll cover additional tax-savings tips for business owners and entrepreneurs.

Step 1: Look for ways to defer taxable income.

Deferring taxable income (which includes accelerating deductions) is usually a good idea, especially in an inflationary environment. It allows you to hold onto your money longer and pay your taxes with devalued dollars later. If we were expecting federal income tax rates to increase soon, we might not be so quick to recommend deferring taxable income, but we’re not Continue reading… Continue reading… Continue reading…

Meet the Team: Client Relations Manager & Marketing Assistant Adela Galeano

Share This Post

We often hear our clients describe SWC as a team as well as a part of their family, and to tell the truth, that’s how our staff feels about the arrangement. Our clients are made up of entrepreneurs and small business owners, real estate investors, and high-net-worth individuals who place a lot of trust in the SWC team/family.

In order to build on that atmosphere, we’re introducing a new series of posts on our blog that spotlights one of our staff members. We’re calling the series “Meet the Team,” and each post appearing under that heading will delve into the qualifications, experience, and perhaps a few personal details about our professional family members.

And we thought the perfect place to start off would be to introduce Adela Galeano, who has been our client relations manager and marketing assistant since 2019.

Adela is highly skilled at managing client relationships and overseeing a number of marketing and administrative functions that keep SWC top of mind. Among these are creating contract-winning proposals for current and prospective clients and working with in-house team members to onboard new clients. On the marketing side of that equation, Adela coordinates our marketing calendars, editorial calendars, and content assignments, as well as updates our client relationship management system that allows us to keep everything well organized and highly responsive.

Adela was instrumental in holding down our San Diego offices during the nearly two-year health pandemic, serving as our office manager when we went remote. She helped our clients by answering the phones and providing a majority of the admin support. Following the pandemic, at a time when many businesses were struggling, Adela took over a multitude of important tasks, enabling our CPAs to concentrate more on our clients.

We sat Adela down for a Q&A session in order to dig deeper into her professional background as well as some pertinent personal queries, and here’s what we discovered:

SWC: What do you want people to know about our tax planning and financial strategy firm?

Adela: I’m impressed at how much our co-founders, Laura and Marni, care about our clients. They give ourclients their entire focus for every email and on every call. They both want to focus on you and you alone, which is why scheduling time on their calendar is so important

SWC: Where were you born and raised, and what did you want to do when you grew up? Continue reading… Continue reading… Continue reading…

Demystifying the Inflation Reduction Act: Part 4 — Additional Provisions

Share This Post

The Inflation Reduction Act of 2022 (IRA ’22) is 750-plus pages of tax and spending legislation designed to tackle everything from climate change to the runaway costs of prescription medication. It contains tax credits for clean energy, nuclear power production, electric vehicles, and other technologies intended to fuel the transition to a lower carbon economy.

It also seeks to reduce health insurance premiums for 13 million low- and middle-income Americans and imposes a $2,000 per year cap on out-of-pocket medicine costs under Medicare Part D. And it establishes a new 15 percent minimum tax on the “book income” of large corporations.

Oh, and if you believe the stated intent, it provides about $80 billion in new funding to the IRS over the next 10 years that is not exclusively for increased tax enforcement. More on this below.

We covered many of the provisions of the new legislation, which the President signed into law on Aug. 16, 2022, in the first three parts of this four-part series:

- Part 1: The Clean Vehicle Tax Credit

- Part 2: Energy Efficiency Credits and Rebates for Residents and Owners of Residential Property

- Part 3: Tax Implications for Businesses and Corporations

Today’s Part 4 of this series covers additional provisions in the IRA ’22 that apply to increased IRS funding, drug pricing, and Affordable Care Act insurance premiums.

Increased IRS Funding

The Internal Revenue Service (IRS) has been underfunded for years. You may have experienced the ramifications of this underfunding if you ever tried to contact the IRS with a question or concern. But the lack of funding has also impaired the IRS’s ability to conduct audits and collect unpaid taxes.

The Inflation Reduction Act of 2022 provides an additional $80 billion to the IRS over 10 years to improve customer services and expand its enforcement and compliance efforts. The Congressional Budget Office estimates that these investments will raise an additional $124 billion from increased collections over a 10-year period.

Perhaps the most controversial aspect of this increased funding is what the IRS plans to do with it — hire and train up to 87,000 new IRS agents. While U.S. Secretary of the Treasury Janet Yellen has indicated that the additional funds will not be used to increase audits of people earning less than $400,000, it would be foolish to believe that such an increase in enforcement efforts would not be used to target regular, everyday taxpayers.

Warning: As soon as the IRS uses the increased funding to become fully staffed, we are confident that it will expand its enforcement efforts to small businesses and households making less than $400,000 per year.

Your best defense is Continue reading… Continue reading… Continue reading…