Welcome to Our Blog

We’re a San Diego, Calif.-based boutique tax consulting firm focused on personalized tax and financial guidance to individuals and businesses. Here on our blog, you’ll find you’ll find news, insights, and observations from trusted sources in the world of tax planning and and financial guidance.

Understanding the American Rescue Plan Act of 2021

Share This Post

On March 11, 2021, the President signed into law the American Rescue Plan Act of 2021 (ARPA) — a $1.9 trillion stimulus package aimed at helping the nation rebound from the economic impact of the COVID-19 pandemic. The Act itself contains more than 600 pages and includes provisions addressing stimulus payments, unemployment benefits, healthcare, state and local funding, along with several tax law changes.

Most of the tax changes are geared toward individual taxpayers, but some affect businesses. In this post, we cover some of the highlights to help you gain a better understanding of the major tax provisions and answer questions you may have.

Getting the Maximum Qualified Stimulus Payment

The big news is the third round of stimulus payments — tax-free money from the federal government. Eligible taxpayers and their qualifying dependents may receive up to $1,400 each. Married couples could receive up to $2,800.

Fewer of us are likely to qualify for the stimulus payment this time around. That’s because the adjusted gross income (AGI) thresholds start at the same amounts, but the phase-out range is much narrower than with prior stimulus payments:

- $150,000 to $160,000 AGI for joint filers, meaning stimulus payments are gradually reduced for joint filers earning a combined $150,000 AGI or more and are not granted to those earning more than $160,000.

- $112,500 to $120,000 AGI for head of household.

- $75,000 to $80,000 AGI for everyone else.

Unlike the prior two stimulus payments, eligible recipients may receive up to $1,400 for all qualifying dependents, including those age 17 and older at year-end.

Tip: The IRS will use the most recently filed tax return to determine these amounts, so do the following to increase your odds of getting a stimulus payment:

- If your 2020 income decreased (from 2019) and is below or within one of the ranges above, file your 2020 return as soon as possible, so that your lower 2020 income will be used to determine whether you get a stimulus payment and how much it will be.

- If your 2020 income increased (from 2019) to a point that disqualifies you from receiving a stimulus check or reduces the amount, consider waiting to file your 2020 tax return until you receive your stimulus payment.

Taking Advantage of the Extension to Unemployment Insurance

The American Rescue Plan Act of 2021 extends federal supplemental unemployment benefits that were set to expire on March 14, 2021. The new law extends the period eligible individuals may receive an additional Continue reading… Continue reading… Continue reading…

Getting Up to Speed on CalSavers: California’s State-administered Retirement Plan

Share This Post

Good news for those of our clients who are employers: California’s new retirement savings plan, CalSavers, may be able to offer your employees the opportunity to save for the future without much effort — and at no cost to you or your business.

CalSavers is available to California workers whose employers don’t offer a workplace retirement plan, along with self-employed individuals and others who want to save extra toward retirement. Savers contribute to a Roth IRA (individual retirement account) that belongs to them but is administered by the state. Employers that don’t offer their own plan simply register with CalSavers by the specified deadline and facilitate their employee’s access to the program.

The program benefits both employers and savers:

Benefits for Employers

|

Benefits for Savers

|

Navigating CalSavers for Employers

All California employers with more than five (5) employees must register for CalSavers by the specified deadline regardless of whether they are exempt from the program. (See below for all associated deadlines.)

Deciding whether you must register

Employers that have at least five (5) employees and don’t already offer a workplace retirement plan can register for CalSavers. Employers that have five or more (5-plus) employees must register, regardless of whether or not they offer their own retirement plan:

- If you already offer a retirement plan, you’re not required to participate in the program, but you must register as “exempt.”

- If your business is a nonprofit, you must register like other businesses, unless it is a religious organization, in which case registration is not required.

- Even if all your employees choose to opt out of CalSavers, you must register if you have at least five employees.

Note: If you’re not required to register and you receive a notice from the state informing you of the need to register, you must respond to the notification to avoid any penalty.

Meeting the registration deadline

If you’re required to register, you must do so by Continue reading… Continue reading… Continue reading…

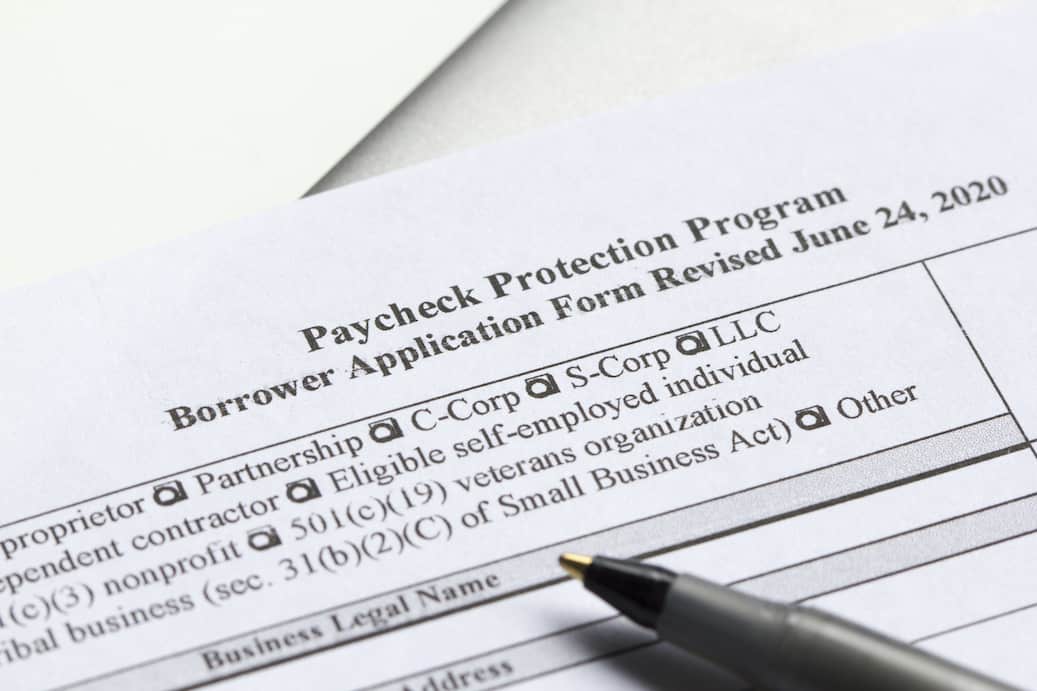

Maximizing Your PPP Benefits and Employer Tax Credits

Share This Post

In 2020, Congress passed a flurry of COVID-19 related legislation designed to help employers retain and pay their employees and stay in business. This relief has been offered primarily in two forms:

- Paycheck Protection Program (PPP): PPP loans have been made available to qualifying small businesses to help them stay afloat and retain and pay as many of their employees as possible. A business receiving a PPP loan can then apply to have the loan forgiven; that is, whatever portion of the loan was used for qualifying payroll and expenses.

- Employer tax credits: Additional employer tax credits have been made available to help employers cover the cost of sick and family leave for employees, employees who need to care for someone with coronavirus (including a child whose school or daycare is closed due to the coronavirus), and retaining employees when operations have been partially or fully suspended due to government orders during the pandemic.

Understanding and taking full advantage of these benefits within the parameters stipulated in the legislation can be challenging for small-business owners. At SWC, we’re here to help.

In this post, we provide an overview of the COVID-19 pandemic relief programs for which your business may be eligible. When preparing your business tax returns this year, your accountant or CPA should be asking you for copies of payroll tax returns and should be initiating additional consultations with you to see if you are eligible for any of the new employer tax credits. We say should because that’s how we handle this at SWC.

Wait! Before You File Your 2020 Tax Return, Read This

Don’t rush to file your 2020 tax returns. Consult with us first for three important reasons:

- Both the PPP and the new employer tax credits provide potentially significant benefits for your business, and we want to make sure you reap the maximum benefit.

- The new employer tax credits cannot be claimed on the same payroll being used for the PPP loan forgiveness. When completing your tax return and submitting documents for PPP loan forgiveness, you need to be sure you’re not confusing the two benefits.

- Your state may not follow all the federal guidelines. We can help ensure that your state taxes account for any differences.

If you feel pressured to file your 2020 tax returns and are uncertain about any of the details related to the PPP or new employer tax credits, we strongly encourage you to file for an extension. With that recommendation in mind, it’s important that you take the time to consult with your tax advisor.

Sorting Out PPP Rounds 1 and 2

Congress provided two rounds of PPP loans — one in the spring of 2020 and another near the end of 2020. If you have taken advantage of the PPP, you should understand the rules and the differences between the two rounds (or “draws.”)

Important: The Coronavirus Aid, Relief and Economic Security (CARES) Act, enacted in March 2020, was silent on whether expenses paid with the proceeds of first draw PPP loans could be deducted. The IRS took the position that these expenses were nondeductible. However, the Consolidated Appropriations Act, 2021 (CAA, 2021), enacted at the end of 2020, provides that expenses paid from the proceeds of both first and second draw PPP loans are Continue reading… Continue reading… Continue reading…

How to Get an Identity Protection Personal Identification Number from the IRS

Share This Post

While con artists love tax season, 2020 marked the first year since at least 2014 that tax-related identity theft was not included on the Internal Revenue Service’s (IRS) “Dirty Dozen” list of tax scams. However, it remains a threat to all taxpayers, yourself included. All the bad guys need to do is file your tax return before you do and redirect your refund to their bank account.

Commissioner Rettig’s words ring true (see image above), especially when you stop to consider that the COVID-19 pandemic has increased online activity for many of us. As a result, it stands to reason that con artists are increasing their online activity as well, and capitalizing on our increased exposure to online identity theft.

One of the tools the IRS offers taxpayers to help in the fight against tax-related identity theft is the Identity Protection Personal Identification Number (IP PIN)— a six-digit number that the IRS is authorized to assign to eligible taxpayers. The number is known only to the taxpayer and the IRS, and it’s meant to prevent identity thieves from filing fraudulent tax returns using the taxpayer’s Social Security Number (SSN).

As the IRS puts it, the IP PIN locks your federal tax account, and serves as the key to opening that account. So, if you file electronically and your submission doesn’t contain the correct IP PIN, it will be Continue reading… Continue reading… Continue reading…

The Potential Tax Implications of COVID-19 Legislation

Share This Post

The dark clouds of the coronavirus pandemic continue to hang heavy over all of us, but even these clouds have a silver lining. The Consolidated Appropriations Act (CAA), signed into law on Dec. 27, 2020, provides for a second round of stimulus payments ($600 per taxpayer and qualifying child), an expansion of the Paycheck Protection Program (PPP), and numerous tax provisions and extensions that benefit both individuals and businesses.

The 2021 tax year brings additional relief in the form of increased contribution limits to retirement accounts, an increase in the standard deduction, and increases in other tax-related limitations and thresholds. (Under our country’s tax code, the standard deduction is a dollar amount that non-itemizers may subtract from their income before income tax is applied.)

In this post, we highlight recent tax provisions, extensions, limits and thresholds you should be aware of as you prepare your 2020 taxes and plan for the coming 2021 tax year.

CAA Provisions for Individuals, Payroll, and Businesses

Consolidated Appropriations Act (CAA) provisions apply to individuals, payroll, and businesses, as presented in the following sections.

Provisions for Individual Taxpayers

The CAA offers the following benefits for individual taxpayers: Continue reading… Continue reading… Continue reading…

How to Get PPP Loan Forgiveness

Share This Post

If you’re an owner or manager of one of the more than 5 million U.S. businesses that received a loan under the Paycheck Protection Program (PPP) — you can now have that loan converted to a grant and forgiven.

However, if you don’t apply for PPP loan forgiveness within 10 months after the last day of the covered period for the loan your business received, then the possibility of deferment ends. At that point, your business will be required to begin making loan payments to your PPP lender.

If your business is a Paycheck Protection Program borrower, it is eligible for loan forgiveness if you used the funds for eligible payroll costs, business mortgage interest payments, rent, or utilities during either the 8- or 24-week period after you received the loan.

Paycheck Protection Program Loan Basics

For the uninitiated, the Paycheck Protection Program (PPP) is a $659-billion economic relief program established as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act to help small businesses, self-employed workers, sole proprietors, certain nonprofit organizations, and tribal businesses remain solvent and continue paying their workers during the COVID-19 pandemic. Under the PPP, a qualifying small business (generally with fewer than 500 employees) could obtain a loan of up to $10 million at a very low interest rate (1 percent) and have the loan forgiven after proving that the money was used for qualified payroll and other expenses.

The following table provides an overview of the PPP Loan program. Continue reading… Continue reading… Continue reading…

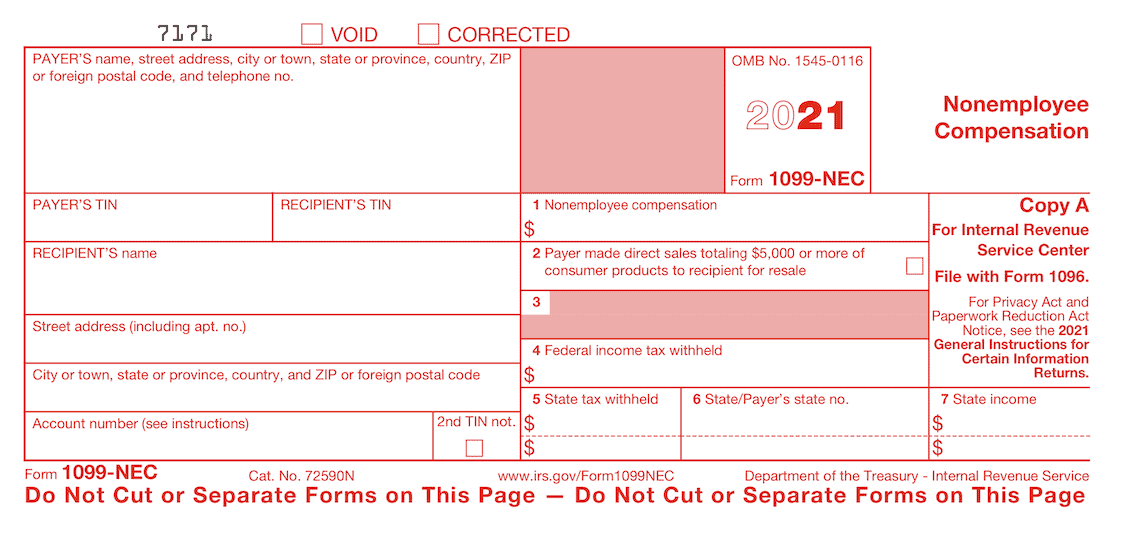

The Return of IRS Form 1099-NEC

Share This Post

Over the past 40 years or so, large and small businesses alike have been using Form 1099-MISC (short for miscellaneous income) to report payments of $600 or more in a calendar year to independent contractors, freelancers, sole-proprietors, and other self-employed individuals. Prior to that, these same businesses used Form 1099-NEC (short for non-employee compensation) for that purpose.

Well, the IRS (Internal Revenue Service) is turning the clock back to the 1980s with the return of Form 1099-NEC.

We can honestly say we didn’t see this one coming. In fact, we thought that the return of Form 1099-NEC was about as likely as, say, a third Bill and Ted movie. Well, we were wrong on both counts. And the funny coincidence is that the return of the 1099-NEC and the release of the third movie (Bill and Ted Face the Music) have both occurred in the same year — 2020, as if this year wasn’t already peculiar enough.

Taking a Closer Look at Form 1099 MISC

Before we look at what changed in 2020 regarding Form 1099-MISC, let’s take a look at what we have all become accustomed to for nearly four decades. Since 1982, businesses that have paid non-employees for their work have issued them a Form 1099-MISC in lieu of a W-2 form (required to report employee compensation).

For the past 38 years, most businesses have been using the 1099-MISC form to report any payments to independent contractors, freelancers, sole-proprietors, and other self-employed individuals who met any of the following three criteria: Continue reading… Continue reading… Continue reading…

Why You Should Schedule a Year-End Tax Projection Meeting

Share This Post

Only two months remain between now and the end of the fourth and final quarter of 2020. Many of us will be happy to be looking back at 2020 in our rearview mirrors, but in regard to taxes — now is the time to start looking forward to 2021 and beyond. The next two months are just as important as the next two years for maximizing your tax savings.

This two-month period is the best time to review any changes in state and/or federal tax law and regulations that could affect how, when, and how much you pay in taxes. During our scheduled tax projection appointment, we will review your current personal, family, and business situations; identify tax-saving opportunities for the coming year; and address any tax questions or concerns you may have.

In addition, if you’re concerned about your tax balance due April 15, 2021, our year-end tax projection can give you a sense of what you can expect to owe or get back in 2020 taxes and consider some year-end techniques that can trim your tax bill or boost your tax refund.

You don’t want to be blind-sided by a tax bill you can’t pay. And if you paid enough (or too much) in estimated taxes, that’s good to know, too — not only for your peace of mind, but also so you can leverage that knowledge for additional tax savings and for your future business and personal financial planning.

Whether you’re a client of ours or another tax planning or financial strategy firm, you should engage in a year-end tax projection session, because the financial decisions and actions you take over the coming months can have a significant impact on your finances for years to come. However, very few people engage in such planning, or they do so without professional guidance. As a result, we suspect that many people miss out on opportunities to Continue reading… Continue reading… Continue reading…

Protecting Your Business Against Theft, Embezzlement, and Fraud, Part 12: Small Business Guide to Reducing Your Tax Burden Legally

Share This Post

Editor’s note: Welcome to the final installment of our 12-part series — “Small Business Guide to Reducing Your Tax Burden Legally.” Admittedly, this final installment is technically outside the scope of this series in that it has little to do with saving money on taxes. However, it does have a lot to do with keeping more of the money you earn as a small-business owner.

Another difference is that we recruited a contributor to write this post — Jen Rodriguez, a Southern California-based forensic accountant with a Master of Accountancy and more than 20 years’ experience in accounting, operations, and data management. Rodriguez is also a graduate of Florida Atlantic University’s Forensic Accounting, Digital Forensics, and Data Analytics master’s program.

Protecting Your Business Against Theft, Embezzlement, and Fraud

By Jen Rodriguez, MAcc

Today’s headlines are filled with stories about small-business fraud, but a vast majority of these stories are about small-businesses committing fraud against the government. Most recently, the news media have focused on fraud involving the Paycheck Protection Program (PPP) — the federal government program designed to keep small businesses solvent during the coronavirus pandemic. The PPP provided ample opportunity for con artists and dishonest small-business owners to defraud the government — and you, the taxpayers — of millions of dollars.

What you hear much less about are the far more common crimes against small businesses, many of which are committed by trusted employees. These crimes include the following:

- Theft: Stealing money or property from the business outright.

- Embezzlement: Diverting money or property from the business for the employee’s own personal use.

- Fraud: Tricking a business into “voluntarily” giving away money or property.

These crimes cut into the profits of any business, but they can be especially devastating to small businesses, and are more difficult and costly for those small businesses to protect against and recover from. In this post, I look at the high costs of these workplace crimes (often referred to as occupational fraud); suggest ways that small businesses can protect against, detect, and recover from these crimes; and highlight the importance of retaining professional services when necessary.

Recognizing the High Costs of Theft, Embezzlement, and Fraud

The U.S. economy is built on the backs of small-business owners, who collectively account for $8.5 trillion dollars of the country’s $17 trillion Gross Domestic Product (GDP). Unfortunately, as we all know, money attracts thieves, and small businesses are often the easiest targets.

Criminal schemes targeting small businesses rarely attract public attention and often go undetected for many years. That’s no surprise given the fact that crimes targeting small businesses are often inside jobs committed by trusted employees. In fact, employees are stealing more than employers are aware. Recent statistics on employee theft reports that 75 percent of employees have admitted to stealing from their employer once, and 37.5 percent have stolen twice.

To protect their businesses and their own financial health, small business owners must Continue reading… Continue reading… Continue reading…

Calculating Tax Withholding and Estimated Taxes, Part 11: Small Business Guide to Reducing Your Tax Burden Legally

Share This Post

Nobody looks forward to paying taxes, but it’s less painful when tax withholdings are calculated by an employer and automatically withheld from your pay. Much easier than crunching the numbers ourselves and then paying the government out of our savings. Somehow, the latter process feels like we’re working for Uncle Sam, and that’s not a pleasant feeling.

Here in the United States, ours is a pay-as-you-go tax system, meaning we taxpayers are expected and required to pay taxes on our income as we earn it — instead of paying it all at once at the end of the year. Employees have taxes automatically withheld from their paychecks by their employers, which satisfies the taxing authority’s requirement.

In contrast, if you’re a small-business owner, you face the onerous task of calculating your income and expenses, estimating the amount of tax owed on that amount, and cutting checks (or making electronic payments) for the amounts due to state and federal entities. These include the Franchise Tax Board here in California, and/or the Internal Revenue Service (IRS). And, you’re required to repeat this process four times a year, to pay your businesses quarterly estimated federal, state, and local taxes.

No one wants to get stuck with a huge tax bill (and penalties) at the end of the year. Nor do we want to overpay, which is essentially giving the government a free loan while leaving ourselves and our business with less of the money we earned. As small-business owners ourselves, we at Stees Walker & Company, LLP, feel your pain, so in this part of our Small Business Guide to Reducing Your Tax Burden Legally — the 11th in our 12-part series — we lead you through the process of estimating your taxes, hopefully making it a little less painful. But first, we need cover a few preliminary topics.

Understanding Tax Withholdings and Estimated Taxes

According to the IRS, “Taxes must be paid as you earn or receive income during the year, either through withholding or estimated tax payments.” Withholdings are taxes an employer collects on behalf of the taxing authorities and sends to them on behalf of the employee. Estimated taxes are generally those paid quarterly based on a business entity’s expected business income. Taxpayers are required to pay estimated taxes in the following situations:

- The amount of income tax withheld from your salary or pension is not enough.

- You receive additional income such as interest, dividends, alimony, self-employment income, capital gains (for example, from selling stock for a profit), prizes, and awards from which taxes have not been withheld.

- You are in business for yourself, in which case the estimated taxes you pay cover not only the income tax you owe but also self-employment tax and alternative minimum tax (if applicable).

If you don’t pay enough tax through withholding and estimated tax payments, you may be charged interest, calculated weekly, on what you should have paid. You also may be charged interest if your estimated tax payments are late, even if you are due a refund when you file your tax return.

To avoid having to pay interest, you must deposit a certain minimum amount by the end of the year: Continue reading… Continue reading… Continue reading…